Crypto Trading Bots for Arbitrage: Complete Guide 2026

with ArbitrageScanner!

Simply put, an automated arbitrage bot will find an opportunity for profit by finding the difference between prices. A number of things will prevent the reliable ability to profit in the short term using the arbitrage business model. These include: the speed that the market moves at (latency), inaccurate allocation (capital allocation) and lack of understanding as to what will occur for a gap in pricing to close. As a result of how arbitrage-style trading bots have evolved, there are now more than enough arbitrage trading bots that have access to WebSocket feeds, the costs of using these trading bots are reasonably priced, and the signals produced by these arbitrage trading bots are of a high enough quality to differentiate those bots that are capable of making money over time compared to those bots whose capital continuously bleeds from the market over time.

This guide will look at the technical workings of arbitrage bots, what you need in terms of your capital to do arbitrage, how to do arbitrage with a detailed example using an amount of capital required to buy from one market exchange and sell from another market exchange (including the detail of how to do this), and lastly, a comprehensive review of the failure points that prevent you from making an arbitrage happen.

What Is A Bitcoin Arbitrage Bot?

A Bitcoin Arbitrage Bot is a trading robot that uses software to identify price differences that exist on many different exchanges. The purpose of a Bitcoin Arbitrage Bot is to identify the price difference of an asset in the market and execute a buy/sell order as a result of the price difference. The primary purpose of an arbitrage program is to execute a trade, by taking advantage of price differences and executing the trade. Unlike other types of automated trading bots which try to take an estimated direction of how an asset will move in the future based on the estimated direction of how the future value would be based on past pricing differences, an arbitrage bot does not take a position on whether or not the asset will go up or down; it solely uses the pricing difference to make a profitable transaction. Because of how you will manage your risk, size your capital, and build your infrastructure, the techniques you will use to trade with an arbitrage trading solution are different from those used in other trading strategies. When engaging in liquid pair trading such as BTC/USDT or ETH/USDT, the arbitrage windows can last anywhere from 30 seconds to several minutes. Smaller capitalization coins will have wider spreads and increased execution risk. A properly configured cryptocurrency trading bot for arbitrage does not operate at regular intervals but rather waits for an opportunity that meets a minimum profitability criterion before responding to that opportunity in an aggressive and decisive manner.

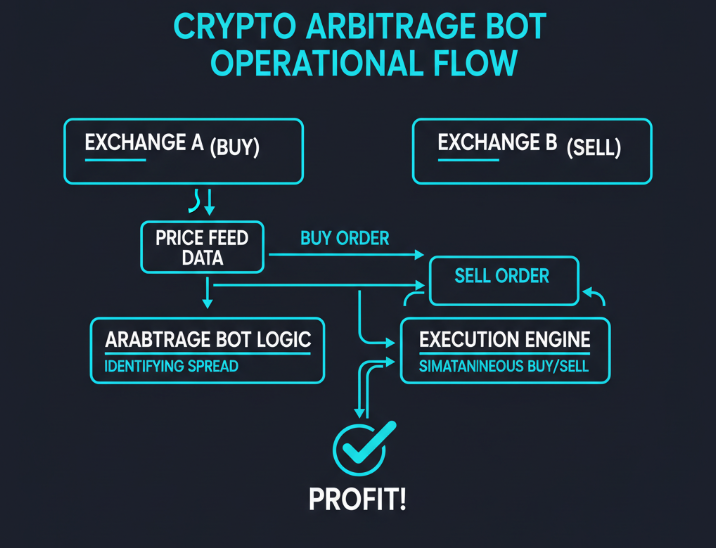

How Crypto Arbitrage Bots Operate: The Math and the Mechanics

Basic Principle: Identifying and Taking Advantage of Spreads

The difference in price between different exchanges is because of fragmented liquidity. The order books on Binance and Bybit are not linked together as they each have their own independent market makers that create liquidity on their respective exchanges and they each have their own individual trader bases and unique fee structures; therefore, when buying interest builds up quickly on one exchange before it can be transmitted to another— an arbitrage opportunity will temporarily open (different price on 2 exchanges for the same coin)

Real-time data quality is what will be the determiner of everything here. A bot that is polling REST APIs every five seconds will always be late to the party because this is structurally late. WebSocket feeds at less than 100 milliseconds latency would be considered baseline operations. Aggregators are providers of a signal feed like ArbitrageScanner that aggregates, merges and filters these types of feeds, looking for spreads that meet or exceed the minimum profit threshold after fees are deducted so that the bot does not execute on empty or short-lived opportunities before any of the initial orders fill.

Processing of Orders: From Signals to Trades

- Identify the Signal — The first step is to have a data feed identify that a spread has opened and qualifies for execution

- Example: ETH/USDT 3,000 on Exchange A, 3,009 on Exchange B (0.30% gross)

- Feasibility Assessment — The bot will calculate the amount of the net spread after deducted the total amounts of maker/taker fees as well as the estimated amount of slippage

- Order Placement — The bot would make simultaneous market orders or aggressive limit orders on both Exchanges

- Trade Confirmed — Upon confirmation that the orders were filled the bot will check for any partial fills and if found it will either abort or hedge out the positions.

- Settlement - This is when funds are sitting on certain exchanges, and how often they will need to be rebalanced by withdrawing from an exchange as-needed.

Mathematical Example: Inter-Exchange ETH Exhibit:

A sample trade will use 1 ETH, the bid price on Exchange A (Binance) is $3000.00 while on Exchange B (Bybit), the ask is $3009.00. This results in a gross spread of 0.30%.

| Item | Amount |

|---|---|

| Buy 1 ETH (a maker trade, has a fee of 0.1%) on Binance | Fees= $3.00 |

| Sell 1 ETH (a taker trade, has a fee of 0.1%) on Bybit | Fees= $3.01 |

| Gross Profit | $9.00 |

| Total Fees | $6.01 |

| Net Profit | $2.99 |

The final calculation results in a net margin of approximately 0.1% against $3000 deployed. The margin is thin, which means position sizing and execution speed will matter most relative to each individual trade.

Types of Arbitrage Bots - Risk/Reward Matrix

| Bot Type | Complexity | Minimum Capital | Average Spread Captured | Primary Risk |

|---|---|---|---|---|

| Scanner-triggered (manual assist) | Low | $500 | .3 – 1.0% | Human Latency in Execution |

| Full Auto (API) Bot | Medium | $2000 | .1 – .5% | API Down Time/Slippage |

| Triangular Arbitrage Bot | High | $1000 | .05 – .3% | Path Dependent Slippage |

| Flash loan arbitrage bots | Very High | Nearly Zero Collateral | .1 – 2%+ | Smart Contract Bugs/Gas Fees |

Note: Values are illustrative only for 2025-2026 marketplace assumptions.

Flash Loan Bots all operate entirely "on-chain" by borrowing capital through a single transaction block, and will be required to repay that capital within the same transaction block. Because of this they require no traditional upfront collateral to conduct trades, however, it is necessary for users to have expertise in writing smart contracts, which adds an increased level of risk in the event that a smart contract has an execution error. Triangular bots utilize arbitrage opportunities through price loops at one exchange only; e.g., USDT → BTC → ETH → USDT. This process eliminates the delay associated with moving funds to other exchanges, however, since the spreads are tighter there are higher transaction fees involved as well.

Minimum Capital Requirements for Arbitrage Bot Trading

The minimum amount of capital trading between two exchanges is $1,000-2,000 when trading on the same pair (e.g. BTC/USDT). Anything lower than this amount will typically have the per-trade fees eat up most of the spread. All of the following must be taken into account.

- Most exchanges have a minimum order size of $10-$5 and meaningful arbitrage trades must have total values greater than $500-$1,500 or more to realize a net profit after trading fees are paid.

- Use a slippage buffer when placing market orders on exchanges with low order book volumes. As an example, by keeping a total position size of no higher than 1% of the top-of-book volume you will minimize your slippage impact from market order placement.

- Cost of rebalancing between exchanges. The cost to transfer USDT between exchanges on a TRC20 blockchain is about $1 per transaction. The cost to transfer BTC between exchanges is 0.0001-0.0005 BTC based on the specific exchange fees you incur.

A more exhaustive analysis on this topic with specific examples can be found in future T4 guides related to capital allocation and rebalancing strategies associated with executing multi-exchange arbitrage.

Recommended Capital Structure for a Profitable and Sustainable Bot Trading Operation

Between $5000 - $10000 spread over two to three exchanges is the ideal ‘working’ amount of pre-funded currency on all three exchanges without incurring wire transfer times between trading activity. This amount will offer sufficient position size in each exchange’s base currency ($500-$1,500 or more) to generate a reasonable net profit on every transaction after trading fees are paid but provide an adequate level of reserves for eliminating (5%-10%) from failure to generate sufficient net profits for maintaining operations.

A more specific method of distributing capital within the arbitrage bot operation assumes the following: 40% of total capital is being used within one exchange for buying; 40% of total capital is being used to sell through second exchange; 20% of total capital is available for re-balancing or transaction fee coverage between exchanges.

Use Case for a BTC/USDT Inter-Exchange Arbitrage Bot

An example of how to use an arbitrage bot is through the use of ArbitrageScanner to monitor BTC/USDT price comparisons between two exchanges, Binance & ByBit.Starting capital of 5k USDT (2.5k on binance and 2.5k in btc on bybit). Step 1 - Signal identification. The ArbitrageScanner detects an opportunity on binance for BTC/USDT at $30k (ask price) and bybit for BTC/USDT at $30,150 (bid price), giving us a spread of 0.50% (gross).

Step 2 - Feasibility check. The total combined fees (binance - maker 0.075% - and bybit - taker 0.075%) equal to 0.15% and estimated slippage of 0.05% gives us a new estimated net spread of 0.50% - 0.20% = 0.30%. Threshold met, proceed with executing the bot.

Step 3 – Execute orders. Buy .0833 BTC on binance at $30,000 = $2,499 (1.87 fee on buy). Sell .0833 BTC on bybit at $30,150 = $2,511.50 sold, ($1.88 fee on sell)

Step 4 - Calculate net profit:

| Item | Amount |

|---|---|

| Proceeds Sale | $2,511.50 |

| Cost Purchase | $2,499.00 |

| Gross Profit | $12.50 |

| Total Fees | $3.75 |

| Net profit | $8.75 |

Step 5- After trade rebalancing activities. After this transaction, the account balances on binance now show three BTC versus zero USDT in the respective account. The account now needs to rebalance funds between Binance and Bybit. The invoices will be sent as a trc20 USDT transfer from binance (cost $1) and the transfer proceeds should balance out to the original initial account holdings. Therefore, the final profit per trade is approximately $7.75 on an investment of $5,000 = 0.155% return per trade.

If 5-10 actionable qualifications occur daily during volatile sessions we would generate an approximate daily amount of $38 - $77. However, if the market conditions were very slow with not much volatility we could produce $0 - $15. Please note: these are not guaranteed returns as that would depend on the market condition at any point in time, uptime of the bot, and available spreads at the time of execution. Also, it would be classified as active management of an infrastructure type and not passive income.

Expected Profit Range (and Failure Modes)

Expected Returns

Here are honest and realistic profit ranges for a properly configured interexchange arbitrage bot operating with $5,000 or $10,000:

Active (volatile) market: Daily volume on invested capital = 0.3% to 1.5% (approximate) Quiet market (low volatility): Daily volume on invested capital = 0% to 0.2% (approximate) Monthly Outlooks: Monthly volume on invested capital = 3% to 15% (highly variable/subject to change)

All of the figures listed are based off of transactional history of the observed BTC and USDT spreads between the two exchanges as of the time period of 2024-2025. Therefore, should there be any changes to the taker fee for any one of the two exchanges or new market participant entering the marketplace or changes to the policy set forth within each exchange; you could have a compression in the spread that would reduce your profitability to an unprofitable level within a matter of days. A change of 0.05% on the taker fee of an exchange would erase the potential for many marginal trades.

Risk and Failure Modes

1. Execution Slippage — If you add a $30,000 BTC Ask You Do Not Have a Guarantee You Will Fill At $30,000

If your exchange has a very thin top of the order book; thus, your buy at 0.1BTC (1/10th of an entire BTC) may fill 0.05 BTC (1/20 th of the entire BTC) at $30,000. Your second 0.05 BTC fill would then fill at $30,005; thereby, no longer having an effective spread.

2. Latency Mismatches — No Guarantees Your Bot Is Executing Both Legs of the Arbitrage Trade Simultaneously (due to latency).

If leg one (the sell leg) fires on exchange A and you are selling 0.1 BTC; but the sell leg doesn't execute on exchange B until 800ms later, the HFT trader on exchange B will have already taken the bid before you have fired the sell leg of your arbitrage trade, resulting in 0.83c net profit instead of the 8.75c profit you would have had prior to leg one firing/executing. This means the original bid of $30,150 may now be $30,100.

3. Beast of an API Error — Your Exchange API will go down during periods of high volatility; whilst at the same time, spreads will be widest and volume will also be the most.

Therefore, when your bot buys from an exchange A and tries to sell on exchange B at the same time (or within the same 10-15 seconds on either exchange) and either fails to perform on exchange B (due to a 503 error) and as a result now has taken on an unintended position. Withdrawal Delays - Transaction Delays. Any UST transfer will take 30-60 minutes to reflect in your account based on the congestion on TRC20 network, even though it takes 5 minutes to physically transfer USDT. Thus, if you run out of your available funds in the process of your session period, you may potentially have less than 5/reg qualifier signals at expiry of your session.

Loss Scenario - Execution Slip - when you place the order for (buying/selling) at time of execution, you will have priced out your arbitrage between both Exchanges at the time of order placement with the execution price of B being $30,050 and A was $30,065 (0.35% spread), with 0.17% spread at the time of execution (300ms real world latency) once the orders have completed. Then, upon netting the difference on the trade ($2,500 = $0.60), you will break-even, as there are no profits from this arbitrage trade at the time of execution. While framing my bid/ask in these trades the API at Exchange A had a throttle and partially filled my order. Upon closing I realized I had lost $1.20 on that trade, and am no longer eligible for a qualifying trade with ArbitrageScanner Signals.

Best Exchanges to use with Arbitrage Bot Strategy

Generally, the best Exchanges to pair with ArbitrageScanner for your Arbitrage Bot Strategy are Exchanges that have: a large depth of orderbook; low-latency APIs; very aggressive maker/taker fee tiers; and highly reliable (or consistent) WebSockets for real time data feeds. For example, Exchange A/Exchanges using the ArbitrageScanner signal include but not limited to: Binance; Bybit; OKX; Bitget; KuCoin; Kraken; Coinbase; Hyperliquid; Drift (On-Chain DEX).

Here are four considerations before investing in the Arbitrage Bot/Strategy:

- Rate Limits (Requests Per Second Per User) on all API calls [rate limits]

- WebSocket Stability/Feed Reliability (Feed drops due to extremely volatile markets) [feed stability]. Fee Tiers Related to Volume - the use of fee tier discounts based on volume are critical to achieving net margin improvement for a maker.

Withdrawal speed/fees - which are the basis for rebalance capital efficiency and overhead- directly relate to achieving effective execution when rebalancing across exchanges.

How ArbitrageScanner compliments Bot-based Arbitrage

Positioned at the intelligence layer of a bot-based arbitrage system, ArbitrageScanner will provide the functionality of real-time monitoring of Net spread levels based on detection across 25+ exchanges and filter based on user defined threshold settings (Net of fees) to prevent bots from chasing invalid gross spreads. The scanner's data can be integrated into a trader's bot via API or custom scripts that will only execute when a validated signal has been produced. For traders using scanner detected signals to drive the bot execution workflow, this will prevent them from having to build and support their own custom infrastructure for collecting and managing feeds from 20+ exchanges. This will result in reducing false signals produced by bots and allowing for faster executions on valid signals. [VERIFY - confirm current API integration format and endpoint availability in ArbitrageScanner documentation]

Conclusion

Cryptocurrency trading bots for Arbitrage are successful when executed correctly; however, the margin for error is very small and the infrastructure required to create these bots must be implemented as defined below. The following is a step-by-step approach to getting started properly:

- Start with a two exchange split of either $2,000 or $3,000, confirm at least 20 executed trades manually prior to automating execution.

- Use WebSocket feeds instead of REST-based polling as latency will be your biggest challenge. Cessation criteria for trading with a bot will involve hard stops and an automatic cessation of trading after three consecutive losses, with the resumption of trading requiring a manual review. In the event the average slippage for each trade exceeds .05%, this indicates the current sizes of trades are excessive relative to the order book depth.

- Use ArbitrageScanner as your signal provider, and apply filtering to it after you verify the net spread, in order to eliminate most of the false positives and to preserve your capital for actual trading opportunities.

FAQ

Will I make money using a crypto arbitrage bot in 2026?

You can; however, in order to earn consistent profits, you will need competitive technology infrastructure, enough initial capital invested ($5,000) and actively develop and maintain your operations. Spreads have generally reduced for larger amounts of most currency pairs (for example, BTC/USDT), although smaller market capitalisation coins still maintain cross-exchange and DEX/CEX spread differences as well as funding rate differentials; and will expect your weekly performance to vary significantly as well, for example there will be some weeks where you will see high levels of activity and others with no activity at all.

Are there legal issues when using a crypto trading bot?

In 2021, using an arbitrage bot on a CEX is legal for the most part as long as you comply with the exchange's terms of service and follow your local regulations regarding market regulations (e.g., Financial Regulation and Securities Exchanges and many others). As a general rule, automated trading will be considered illegal if market manipulation occurs through layering, spoofing or wash trading; before trading, examine each exchange individually and engage another party to review your compliance with all market requirements if you will be trading using institutional size orders.

What is the minimum amount of money that I would need to trade with an arbitrage bot?

Minimum operational size of capital needed will be $1,000 - $2,000 for each exchange trading pair you obtain, and $5,000 - $10,000 will be a sufficient amount to open your trading account, if you want your operations to be sustainable and to earn meaningful profit from them. If you are using capital below $1,000, you will probably lose most, if not all, of your spread due to slippage and commissions for each trade that would meet the minimum order limits imposed on you by the exchange.

Can a crypto arbitrage bot lose money?

Yes; because of slippage, latency issues, partially filled orders, down-time of your API, and material price movement on your orders between the time you placed your orders and the time your orders were executed, you may incur a negative gross spread of, for example, -0.05% as opposed to your anticipated gross spread of 0.30% due to your order execution timing delays. In addition, you could also acquire unintended open positions due to incorrectly configured parameters, missed maintenance periods or wrong API permission configurations.

What criteria should I use to select a crypto arbitrage bot?

Evaluate the arbitrage bot using the following four criteria: (1) Execution latencies - for roundtrip execution times <200 ms is the competitive threshold; (2) Exchange coverage - does the bot connect to the exchanges where you will be looking for possible arbitrage; (3) Fee calculation accuracy - does it calculate correctly the proper tiers of maker & taker, withdrawal fees and network trading commissions before generating a signal for you to execute a trade; and (4) Quality of Signal - does it connect to a real-time spread provider such as ArbitrageScanner or does it generate its signals through a polling based method; and therefore in contradiction to the standards for providing you with a real-time signal?

Want to learn more about crypto arbitrage?

Get a subscription and access the best tool on the market for arbitrage on Spot, Futures, CEX, and DEX exchanges.

You might be interested

Binance for Arbitrage: Complete Guide 2026

Binance-Bybit BTC Arbitrage: Spread Patterns, Fees and Execution Guide 2026

Funding Rate Arbitrage Explained: Complete Strategy Guide 2026