Funding Rate Arbitrage Explained: Complete Strategy Guide 2026

with ArbitrageScanner!

Arbitrage of funding rates through cryptocurrencies involves making money using the mechanics associated with perpetual futures contracts, regardless of price direction predictions made by others. For example, to make yield through ‘arbitrage’, you could buy an asset on the spot market, short an equal amount of its notional value using perpetual future contracts, and collect payment each eight hours from supply and demand when positive funding rates exist while using a neutral position based on value of funds flowing from long sides of market. As position offsets therefore, any loss from increasing price due to BTC rising up to 15% is offset by gains associated with notional value gained from a negative future short and vice versa and therefore net profit and loss associated with 8% to 20% annualized rates based upon effective execution in each instance dependent upon (1) current market stability with respect to positive funding rates or (2) persistent negative funding rate in bear markets. The guide will cover the mechanics associated with arbitrage, annualized rate math calculations, provide a working example step-by-step with regards to how an order can be filled through Binance and specify how the order could vary significantly depending upon failure to complete arbitrage long-side positions within a timely manner.

What is Arbitrage of Funding Rate?

Perpetual future contracts have no expiration dates, creating a fundamental issue in determining how to price contracts; thus, pricing is determined by settlement at either a spot or via a funding mechanism. Each eight hours, the two sides of the perpetual market will derive a funding rate from paying one another.

- If long positions exceed equivalent spot value (i.e., positive funding position), therefore creating both payment and cashflow obligation from long to short position.

- Conversely if short positions exceed equivalent value based upon spot, therefore creating both cashflow obligation and funding obligations being owed from short -long position to short or long. "Within the perpetual futures contract, there is an equivalent notional value short on the prices of asset (shorting). The two positions offset each other, meaning that the portfolio collects funding payments on the short side of the position each time they settle without assuming any directional risk provided the hedge continues to be effective."

The funding rates for perpetual contracts (Binance, Bybit, and OK) are calculated on a periodic basis (every 8 hours) via two inputs: the premium index, which represents the difference between the mark price of the perpetual and the spot asset's index, and a fixed interest rate component (0.01% per 8 hours in USDT-M on Binance) used to establish a baseline for further adjustments to the funding rate when there exists an average premium in the mark price to spot during periods of sustained "bull" sentiment.

An analysis of the historical monthly average funding rates on Binance BTCUSDT perpetual indicates a historical variance in rates from -0.05% to 0.10% at the end of the time periods referenced with averages typically clustering around 0.03% to 0.08% over the course of weeks during the last portion of 2020, the middle part of 2021, and the last part of 2023. In contrast, the funding rates averaged less than -0.010% over an extended period during the bear market in 2022.

In order to convert a period funding rate into an annualized percentage yield (APY), follow these steps:

- Funding Rates per day: (3).

- Funding rates per year: 3 x 365 = 1095.

- Formula:

APY = (1+r)^(N) - 1.

For instance, at a fixed funding rate of 0.01% per 8 hours: ((1.0001)^^^(1095) - 1 ~ 11.50% APY). If only a moderately bullish sentiment exists, funding rates at 0.03% or greater during period funding intervals of 8 hours will bring an annualized gross APY of approx 39%. The current (elevated speculation) 0.05% funding rate per 8-hour window will yield a gross APY of about 71%, but these periods have a shorter lifespan than typical and carry an exceptional level of reversal risk.

After accounting for fees and slippage, as well as periods of zero or negative funding, target realistic net APY's are significantly lower over the duration of a full market cycle. When conditions are favorable, expect a net APY of 10-15% and in neutral markets, 0-5%.

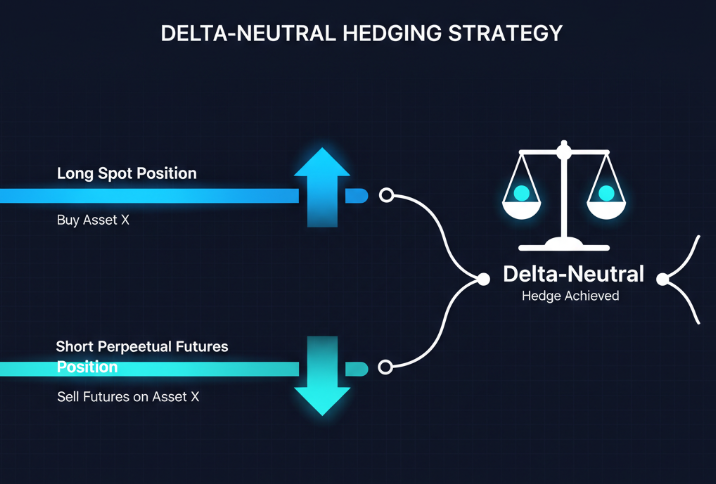

Delta-Neutral Hedging

A long BTC position at $10,000 and a short BTCUSDT perpetual at $10,000 are delta-neutral when initiated. That is important because as the price of BTC changes, the dollar value of each leg of that position will change as well. If the price of BTC rises by 20%, then the long will increase to $12,000, while the short anchor will still reflect its original value (or will move inversely). Over time, without rebalancing, that delta will accumulate unintended directional exposure. Review the delta once weekly and rebalance if it exceeds ±5% of the original notional amount.

Required Capital

Minimum and Recommended Amounts

While this strategy can be executed with as little as $1,000 in capital, it is economically infeasible to execute with less than $5,000 in capital. Opening and closing both legs of a trade includes futures and spot commissions (Binance V0) — approximately 0.2%–0.3% of the notional value of the completed trade — and since current funding rates average approximately $1.50 per funding period for $2,000 in capital, several days' worth of yield will be consumed by day one commission costs.

Minimum workable capital: $5,000. With that amount, you will have approximately $45 -$90 of gross yield per month based on 0.03% average funding rates. This will cover commission expenses and provide a sufficient signal on whether or not your position has been profitable. Minimum Working Capital: $10,000 to $25,000. The minimum recommended working capital for this strategy is $10,000 to $25,000. The working capital range allows you to pay a smaller percentage in fees on your yield, easily execute trades across the liquid BTC & ETH pairs, and your management of your positions is simplified. If you have more than $50,000 in working capital, you may qualify for an additional tier of fee reductions, which can increase your overall net returns by 20%-35% compared to VIP 0.

Asset Allocation

Use a 50/50 Capital Split between your Spot Wallet and your Futures Wallet. For this strategy, leverage should be used at 1x (short side). Therefore, your margin in your Futures Wallet will be equal to your short notional. When shorting in the Futures Wallet, do NOT use 2x or greater, as the funding yield is where the edge of this strategy lies, and therefore the use of leverage will only add risk of being liquidated and will have no effect on your funding capture rate.

Example Trade — Binance USDT-M + Spot

Situation: BTC Funding Rate (Binance USDT-M) 0.03% average every eight hours; Capital: $10,000; All Trades Executed at Market.

Step 1 — Fund Accounts. $5,000 USDT into Binance Spot Wallet, $5,000 USDT into Binance USDT-M Futures Wallet.

Step 2 — Purchase Spot BTC. $5,000 USDT purchase on Spot BTC. $65,000/BTC purchase 0.0769 BTC. Spot Taker Fee $5,000 * 0.10% = $5.00.

Step 3 — Open Perpetual Short. Short Sell 0.0769 BTC on BTCUSDT Perpetual for a total Notional Value of $5,000. At 1x Leverage, $5,000 margin is required. Futures Taker Fee $5,000 * 0.04% = $2.00.

Step 4 — Monitor Funding. Funding settles on the hour every eight (8) hours from 00:00 UTC, 08:00 UTC. Under the terms of 0.03% financing rate each time you receive payments of $5,000 × 0.03% (3 different payments), you will receive $1.50 on each payment as the funding from the short position that you will be getting.

We have now progressed through the next steps of trading using BTC Futures:

5. You will receive a total of $135.00 in gross total payments over this period (30 days/ 3 payments/day) for receiving funding while you hold your long future in BTC.

6. Each week you will assess the difference in value between BTC spot price and the BTC Futures Value (Notional Value). If BTC were to drop 15%, you will realize an approximate profit ($750.00) when closing your position to enter your long futures (you will also incur an approximate loss of $750.00 on your long spot purchase). To liquidate a short position, the value of BTC at the time you entered your position must have decreased by 85% — hence it would need to decrease in value by 85% or more before you can liquidate your position.

7. The closing of the futures position occurs when you sell spot market to take on the BTC long position at a price of $5.00 when you sell BTC short for $2.00 = cost to exit short position = $7.00.

So the total net profit from the 30 day hold for the $10,000.00 position = total gross profit ($135.00) – total fees $14.00 = total net profit ($121.00). Therefore, you can expect approximately a 1.20% monthly return from each $10,000.00 position.

Example Table Based On 0.03% Average Funding Rate With 30 Day Hold, VIP Tier 0 Fee, Market Order Only:

| Total Capital Deployed | Gross Funding Amount For 30 Days | Total Round Trip Fees | Total Net Profit | Total Net Monthly Return |

|---|---|---|---|---|

| $5,000 | $67.50 | approx $7.00 | $60.00 | approx 1.20% |

| $10,000 | $135.00 | approx $14.00 | $121.00 | approx 1.20% |

| $25,000 | $337.50 | approx $35.00 | $302.00 | approx 1.20% |

| $100,000 | $1,350.00 | approx $140.00 | $1,210.00 | approx 1.20% |

NOTE: The above data represents hypothetical Profit; the actual Profit/loss would differ based on funding rate, and/or slippage, fee tiers, and execution quality. Tiers of Higher Capital Mentions May Qualify for Lower Taker Fees, Leading to Higher Returns. #TODO: Link Candidate→Article on Binance Fee structure, VIP Tier calculation for Arbitrage

Realistic Profits Ranges

During full-market cycles, Delta-neutral Funding Arbitrage between BTC and ETH on large exchanges Generates an Annual Return of 8% – 20% in Sustained Positive Funding while Narrowing to 0% – 5% During Choppy or Sideways Markets And Creating Negative Returns During Long Drawn-out Bear Market Phases Where the Funding Is Below the Break-even Fee Threshold (approximately 0.007% every eight hours On Binance For VIP 0)

As amounts increase to $100,000 or More, Lower Fees Create Up to 30% – 40% Less Drag On The Returns and Institutional Desk Volume, Can potentially Narrow this Further. Additionally, this does not compound by itself; profits must be redeployed actively.

The losing scenario occurs when the average funding rate is = −0.01% every 8 hours for BTCUSDT over subtended periods during 2022. A $10,000 position was $90 in funding received as the long side and approximately $14 in fees incurred—an approximate total loss of $104 on a $10,000 position opened. Neither Long, Short / or Held Within A Funding Environment was Negative

Operational Risk and Emergency Closing of Funding

The largest operational risk is the movement and Rate Change of Funding. For example, the Spot Rate Could change From +0.03% to From 0.01% in Just a Few Hours Based on Mass Deleveraging Events. CoinGlass Historical Data Shows BTC Funding Rates on Binance Were In The Negative Approximately 20%-25% of 2022-2023. Positions that are Managed through these periods, Without Close Monitoring Will Continue to Accumulate Losses Quietly. If you experience a continued downturn in funding, set a one-time alert when it falls below your cost to cover fees and exit within that one funding cycle if the trend continues.

Risk of Liquidation

When using a 1x leverage on BTC or ETH, to incur a liquidation means that the price of the asset has dropped 85% or more - so this liquidation process is not significant to risk for you. The real risk for liquidation comes from traders utilizing cross-margin accounts. These accounts pool together the funding arbitrage short position as well as any other leveraged position that the trader currently has on. If a trader has entered into a long position on another asset, and that asset becomes liquidated, the collateral used for the arbitrage short position can be taken into account by the long position and forced out of the market before the trader has a chance to sell their position at the current market price. Therefore, to keep the arbitrage short safe and separate, isolate the margin for that arbitrage short position.

Exchange Counterparty Risk

Major exchanges have been insolvent, frozen users funds (stopped allowing withdrawal of funds), and had system down time that lasted for several days. Placing the entire position - spot + future contract - on the same exchange creates an additional layer of risk. In the event an exchange suspends withdrawals and you have both legs of the trade on that single exchange, you could find yourself stuck in a position that cannot be exited unless you agree to sell your position below the market price. Spreading your exposure to two different exchanges will introduce basis risk, but will also limit your exposure to one point of failure.

Slippage and Fee Drag

On BTC and ETH using Binance or Bybit, slippage on a market order of $25,000 is generally less than 0.05% of the trade amount, making slippage negligible as compared to the fee dragged on a market order of similar size. However, on illiquid smaller cap assets, slippage could exceed a full day of yield in the funding rate on a market order of the same size. To rid yourself of slippage, you should focus on the top 20 coins by open interest and refrain from trading on the long-end of the spectrum only.

Imperfect Hedging and Basis Risk

The USDT perpetual contract and USDT spot prices traded on Binance track closely to the same index and therefore there is no active basis risk as you would have when hedging in the short-term and shorting/going long, spot market on Binance. During periods of market stress on the respective exchanges, there is a high degree of "basis risk" associated with maintaining cross-exchange/perpetual-exchange hedged positions. Price divergence can exist for short durations and create an unexpected P&L on these supposedly neutral positions.

Regulatory Risks

Regulatory agencies in different countries impose varying degrees of restrictions on the trading of perpetual futures through both exchange limitations and enhanced KYC obligations. As a result, a regulatory agency may suddenly impose new restrictions on a platform without any prior notice, which may result in an unanticipated exit from your positions at an unintuitive price.

The Best Exchanges to Execute on the Strategy

To achieve the desired level of effectiveness, funding rate arbitrage trades should be executed on exchanges that have deep perpetual open interest, have competitive taker fees for the placement of orders, and have reliable/robust withdrawal and cash withdrawal infrastructures. The exchanges most suitable for the execution of this strategy in an active perpetual futures contract environment are Binance, Bybit, OKX, Bitget, KuCoin, HTX, MEXC, BingX, and Hyperliquid. When executing on-chain with transparent execution mechanics, consideration could also be given when determining the best exchanges to support this type of trade to prefer Drift Protocol (Solana). The selection of the platforms should have the listed criteria: asset pairs that are available on each platform that have a historical record of consistent positive funding payment history, futures exchange fee tiers (higher tier = higher fees to cancel long/short futures), USDT cash withdrawal fee levels, and stable/usable API access for the purposes of system automation and constant monitoring.

ArbitrageScanner.io is the only website that provides live updated funding rates by exchange for cryptocurrency trading through a single user interface. Through use of ArbitrageScanner, traders executing on this funding rate arbitrage strategy can view current funding rates on a per-asset and per-exchange basis, as well as view historical funding rates simultaneously; and customize alert notifications to each user when funding rates. In addition, through use of the ArbitrageScanner cross-exchange comparison tool, traders who maintain multiple delta neutral positions will no longer need to monitor each individual platform. If the prices soar on a secondary exchange, then most traders will not be able to enter until after the alert system is activated; this gives you a significant edge or discrepancy from others who may also have been waiting on their entry but have missed out due to the delay between activation of alert and response time to enter at the new price.

The overall profitability of arbitrage is primarily dictated by having a well-disciplined process (as opposed to utilizing one's market expertise). Operational mistakes will ultimately cost you much more than mechanical errors.

- Start small ($10,000 or less) so that you can understand all of the mechanics of arbitrage before you scale up your funds. The larger the amount of money you have mismanaged, the more significant your loss will be.

- Always trade futures shorts using isolated margin — meaning that you should never combine your arbitrage trades (which utilize leverage) with any other type of directional trade (which will also utilize leverage) in the same margin account.

- Have an alert on your funding rate so that when the rate falls below the break-even point (which you can calculate by multiplying the trading fees you pay to Binance and dividing that amount by the number of hours your long position has been held) and for 2–3 consecutive funding cycles of negativity, exit your position.

- Rebalance your portfolio every week to ensure that your spot and futures notional values are within 5% of each other; anything outside this range opens your trade(s) up to directionality.

- Evaluate your portfolio every quarter rather than every month because the environment for funding rates will change according to market conditions. A single month's negative funding does not cancel the validity of your arbitrage strategy; four consecutive quarters of negative funding do.

FAQ

Is financing rate arbitrage risk-free?

No! When done properly, this strategy will eliminate most of your directional price risk. However, it does introduce different types of risk (funding rate reversal risk − paying instead of receiving − exchange counterparty risk, margin management risk, and fee drag). In addition, losing money from having prolonged periods of negative funding paired with entering and exiting your position will result in real losses. In general, "delta neutral" does not mean your capital is safe.

How often are funding rates paid?

Funding rates are settled every 8 hours (00:00, 08:00, 16:00 UTC) on Binance, Bybit, and OKX; while funding rates are settled hourly on Hyperliquid and some of the newer DEXs. The higher settlement frequency results in faster accumulation of yield when the rates are positive and of losses when the rates are negative.

What is "delta neutral" in relation to funding rate arbitrage?

Delta neutral means that the portfolio has a net sensitivity of approximately zero to the underlying asset's price movement. A $10,000 long spot position and a $10,000 short futures position in BTC would have their changes in value offset each other if the price of BTC increased by 10%; therefore, the net value for both would be close to zero (the spot position will have increased by approximately $1,000 and the futures position will have decreased by approximately $1,000). Therefore, you earn money from funding payments rather than from directional price movement, but you incur costs from funding payments when rates go negative.

Is it possible to lose money with funding rate arbitrage?

Yes. One of the most obvious scenarios for this would be if funding rates go negative for an extended period of time. In a 30-day period, a $10,000 position with an average funding rate of −0.01% would incur a payment to the other side of $90 + approximately $14 in total round-trip fees. This would result in a net loss of around $104 without requiring any type of directional exposure at all. This type of scenario occurred frequently during the bear market for BTC and ETH perpetual markets from 2022 until 2023.

Which exchanges are the best for funding rate arbitrage?

The best exchanges to consider for funding rate arbitrage would be Binance and Bybit. They have the largest perpetual open interest and the largest liquidity in BTC and ETH markets. If you are executing trade sizes in the mid-range, then OKX and Bitget have competitive fee structures. If you are executing on-chain with real-time transparent information about funding rates, then on Solana, Drift Protocol. The best option will differ depending on the asset traded, the capital tier of the trader, the negotiability of fees, and whether cross-exchange comparisons will be necessary which is what ArbitrageScanner does in real-time.

Want to learn more about crypto arbitrage?

Get a subscription and access the best tool on the market for arbitrage on Spot, Futures, CEX, and DEX exchanges.

You might be interested

Impermanent Loss Explained: What Every DeFi Liquidity Provider Must Know in 2026

Crypto Trading Bots Comparison: 20-Day Profit Challenge

SMT Divergence