Impermanent Loss Explained: What Every DeFi Liquidity Provider Must Know in 2026

with ArbitrageScanner!

DeFi produces very attractive yields that entice liquidity providers (LPs) to provide liquidity in exchange for high returns. There is though, a risk that often goes unnoticed; that being the risk of impermanent loss (IL). Many LPs do not fully understand how IL will affect them when they provide liquidity to a pool which can result in substantial losses due to poor decision making about when to withdraw capital. This guide aims to demystify IL for LPs by explaining IL, how it works, and how to manage it to maximize profitability in DeFi through 2026.

Understanding Impermanent Loss

IL is defined as the difference between the value of the assets held as part of a liquidity pool in an Automated Market Maker (AMM) versus holding the assets in a wallet. IL exists due to the price ratio between the two tokens in the pool changing after the tokens are deposited into the pool. As long as LPs do not withdraw their liquidity before the asset prices revert back to their original price ratio, there will be no actual loss of capital due to IL. When asset prices revert back to their original price ratio, the actual extent of IL that an LP has experienced will be eliminated.

IL is entirely driven by how AMMs operate, particularly through the use of the constant product formula (x * y = k). When one asset in a pair of tokens experiences a relative change in price, the price of the other token will still remain the same, or stay at a different price, relative to the first token, resulting in arbitrageurs entering and exiting the pool to bring the pool back into alignment with the prices of the two tokens as they are on the outside market. As a result, when LPs provide liquidity to the pool, they end up with more of the token that has depreciated in value compared to what they would have by holding both tokens separately. The volatility of the crypto market is the primary cause of IL.

Let’s illustrate this with a simple example:

- You deposit $1,000 into the ETH/USDT automated market maker pool with 0.25 ETH ($500) and 500 USDT ($500) at the time where the price of 1 ETH was valued at $2,000.

- At a later date, if the price of ETH increased to $4,000, there will be arbitrage opportunities (prices vary from one market to another) for arbitrageur’s (traders that exploit price discrepancies) to buy ETH out of the automated market maker pool. This reduces the number of ETH in the pool and increases the number of USDT in the pool in a way that results in the new price of ETH ($4,000) being reflected in the pool’s ratio of ETH to USDT.

- As a result, your share of the pool would now be 0.176 ETH ($704) and 707 USDT ($707), which is equal to the total of $1,411.

- However, if instead of providing liquidity you would have left your assets held in your wallet, you would have 0.25 ETH ($1,000) and 500 USDT ($500) in total value ($1,500).

- Therefore, the impermanent loss you will incur when you later withdraw from the pool as a result of your prior deposit will be $1,500 - $1,411 = $89.

The fundamental step-by-step calculation associated with a loss of this nature is required in order to understand how such a divergence loss occurs. The automated market maker has an inherent design flaw that is caused by the use and adherence to the automated market maker’s invariant constant product formula where the ratio of the assets held in the automated market maker pool periodically vary as a result of external price fluctuations.

Consider the activity in the pool based upon the following token pair – ETH and USDT.

Initial Deposit Activity

Let’s define the Initial state of the pool as follows:

- The automated market maker pool now contains a total of $2,000 worth of assets (1 ETH = $2,000).

- To add to the total value within the automated market maker pool you deposit a total of $2,000 in the pool consisting of 0.5 ETH and 1,000 USDT.

- Assume the configuration of the automated market maker pool prior to your liquidity event contains 10 ETH and 20,000 USDT. Therefore the constant product ‘k’ for determining the balance of the pool is equal to 10 * 20,000 = 200,000.

- LP Ownership % - The LP participant would own 5% of the pool (0.5 ETH / 10 ETH equals 5%).

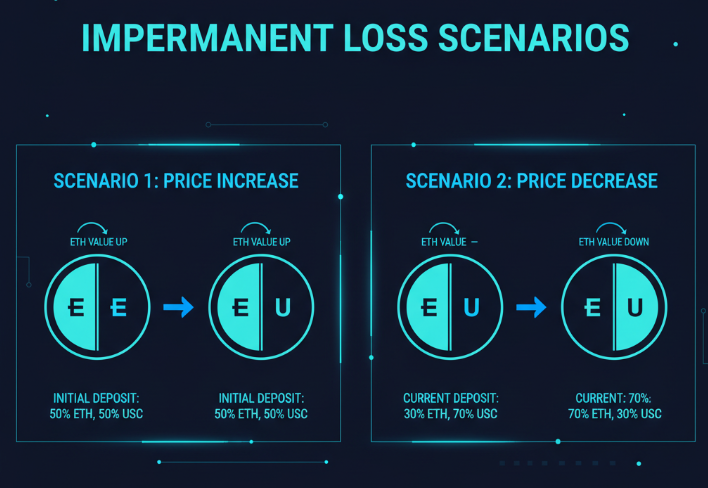

Scenario 1 - Price of ETH increases dramatically

The price of ETH has had a large increase resulting in the liquidity pools rebalanced.

- New price of 1 ETH would equal $4,000.

- Arbitrageurs can buy ETH at the pool level with USDT till the pool is in line with the market price.

- The new configuration of the liquidity pool will contain approximately 7.07 ETH and 28284 USDT (7.07 X 28284 = approximately 200,000).

- The LP still will have ownership of 5% of this liquidity pool or 0.3535 ETH and 1414.2 USDT.

- If the LP would have held these funds separately the value of the held 0.5 ETH would equal $2,000 and the value of the held 1000 USDT = $1,000. Therefore the total is $3,000.

- However the LP share of the total portion held in the pool is calculated as follows: 0.3535 ETH x $4,000 equals $1,414 and 1414.2 USDT = $1,414 and total value is $2,828.

- Thus the LP has incurred $3,000 (held) - $2,828 or $172 as impermanent loss that represents a 5.73% impermanent loss to held value.

Scenario 2 - Price of ETH decreases by 50%

The price of ETH will decrease, resulting in a different configuration of the liquidity pool.

- New price of 1 ETH will equal $1,000.

- Arbitrageurs will sell ETH to the pool for USDT until the pool has been reconfigured to equal the market price.

- The liquidity pool will now hold approximately 14.14 ETH and 14,142 USDT (14.14 X 14,142 equals approximately 200,000).

- The LP still has 5% ownership in the pool, thus the LP will have an ownership of 0.707 ETH and 707 USDT.

- The Value Held Alone: 0.5 ETH ($1,000) = $500; 1,000 USDT = $1,000; Total = $1,500

- The Value in Pool: 0.707 ETH ($1,000) = $707; 707.1 USDT = $707; Total = $1,414

- Impermanent Loss Calculation: $1,500 (Held) - $1,414 (Pool) = $86 Impermanent Loss, which is 5.73% (vs. value of assets)

Impermanent losses are always caused by differences in price between prices of assets held and traded. LP Tokens give members a proportional share of their pool’s assets as liquidity providers; however, all members’ shares have value based on how the price fluctuates.

Helps to visualize with Table:

| Metric | Starting Condition (1 ETH=$2,000) | 1 ETH = 4K (Double Price) | 1 ETH = 1K (Half Price) |

|---|---|---|---|

| Value Held Alone | 2K | 3K | 1.5K |

| The Value In A Pool | 2K | 2.83K | 1.414K |

| Amount LP Is Losing | 0 | 172 | 86 |

| Percentage LP Is Losing | 0% | 5.73% | 5.73% |

The Trade-Off Between Fees And Impermanent Loss As A Liquidity Provider

The majority of liquidity providers' motivation for providing liquidity to the pool comes from the fees they earn from transactions executed by using the liquidity generated from their respective liquidity deposits. As liquidity providers, each provider is entitled to receive a portion of total liquidity fees earned based on the amount of liquidity they provided. It is essential to determine whether or not a DeFi farming yield strategy’s total transaction fee revenue will exceed the total amount of impermanent loss.

Trading Fees

- Creating a Fee: Making a trade with an automated market maker (AMM) incurs a small fee per swap, typically between 0.01%-0.53%. An example of this includes Uniswap V2's pools which charge typical transactions 0.7%.

- Volume Matters: Increased volume within a single liquidity pool will translate to an increased amount of fees for Liquidity Providers (LPs) – volume is a strong indicator in whether significant profits will be made over time for the LPs.

- Pool Size: All fees will ultimately be split amongst all LPs in the same liquidity pool, which means that the smaller the liquidity pool, or the larger LPs share in a liquidity pool, the greater amount (percentage) of fees will be distributed to that LP.

Balance

The ability of a liquidity provider to be profitable is dependent upon the interaction between the liquidity fee and impermanent loss.

- Offsetting IL: In some cases, your liquidity fees will partially or fully offset any impermanent loss you experience with the price volatility of the liquidity pool token being traded. If there has been significant volume over a short period of time and moderate price volatility in this pool, your fee income may easily exceed your impermanent loss.

- LPs Aren't Profiting: In other instances, the opposite will occur — that you will not be able to cover your impermanent losses through trading fees. This can occur when there is extremely high volatility in the price of both tokens of any pair being traded on a liquidity pool. The impermanent loss will far exceed the trading fees you earned as a result of the trading volume of that pair. This is one of the major risks associated with providing liquidity.

- Breakeven Point Differentiation: LPs have a desire to earn fees equal to their impermanent loss through trading to reach what is known as the "breakeven point" of providing liquidity. The use of an impermanent loss calculator can help LPs to understand if or when they will be able to reach the breakeven point.

As an example, if an LP has incurred a 5% impermanent loss on $10,000 of liquidity, this means he or she has lost $500 equivalent to his or her position in the pool. If the liquidity pool generated $1,000 in trading fees over that same time frame, then he or she would have a net positive cash flow of $500 ($1,000 – $500 = $500) from his or her liquidity position. While a pool with just $300 worth of fees would give an LP a net loss of approximately $200, it is critical to choose a pool with a balanced level of expected volatility and expected trading.

Concentrated Liquidity and Impermanent Loss in Uniswap (and Other Evolutionary AMM Variants)

The innovative structure of concentrated liquidity (CL) developed in the Uniswap V3 design has fundamentally changed the way AMMs (automated market makers) function. In traditional AMM models, the liquidity providers (LPs) are required to supply capital to ALL possible price ranges from zero to infinity. By contrast, the CL design allows LPs to select specific price ranges within which they would also prefer to supply their liquidity. This innovation increases the efficiency of the use of LP capital but also provides for a new set of operational dynamics with respect to the risk of experiencing impermanent loss.

Advantages of Concentrated Liquidity

- Higher Capital Efficiency: Compared to traditional AMMs, LPs will now be able to provide equivalent depths of liquidity to a market with far less capital because LP capital is concentrated in the area of highest trading activity, rather than distributed thinly across a range of prices where there is very little active trading.

- Maintenance of Higher Fee Revenue: LPs will generate a higher proportion of the fees related to activity in any relative liquidity pool than they would have in a traditional AMM because their capital will be more actively utilized in supporting the trading activity in that pool.

- Flexible Capital Allocation: LPs will have the flexibility to choose the 'width' of their selected liquidity support ranges based upon their outlook for the prices of the underlying instruments.

Increased Risks Require LPs to Provide Active Asset Management

Although LPs can utilize a high level of capital efficiency by providing concentrated liquidity, the potential for LPs to experience impermanent loss (IL) is also magnified by the concentrated nature of the provision of their capital. Some of the risks related to LPs that arise from the provision of concentrated liquidity include:

- Out-of-Range Risk: LPs may experience IL if the price of the token pair traded is currently outside the range of prices the LP selected. The current position of a Liquidity Provider (LP) only has holdings of a single asset and will not receive any fees until prices return to normal. Because of this, the LP will have a large amount of impermanent loss that will be locked in.

- Since concentrated liquidity requires active management (as the LP is required to watch the movements of a coin's price and alter their ranges in order to earn fees), there is the cost of gas associated with rebalancing their position.

- When prices swing rapidly, an LP may also experience much more drastic impermanent losses due to their concentrated position than if they were to have provided liquidity over an entire range of price. This is primarily due to LP's capitals (100%) being fully exposed to the price difference within their narrowed range of coverage. This range is typically much smaller than the overall market.

To illustrate the above, let’s assume that LP has provided liquidity for ETH/USDT between $2500 and $3500. LP would typically earn a significant amount of fees while there is trading occurring between these amounts.

If the price of ETH were to drop to $2000, then LP would have a concentrated position at 100% in ETH and so the LP would earn no fees and have considerable impermanent loss. LP would have substantially more ETH now than had an LP invested in his original assets.

If the price of ETH were to rise to $4000, then LP would have a 100% USDT concentrated position and so earn no fees along with again having large impermanent losses.

This exemplifies that while LPs have more potential return available to them with concentrated liquidity, they will require significantly more understanding of how the overall market operates and also have to actively manage their impermanent losses.

Strategies to Mitigate and Hedge Against Impermanent Loss in 2026

It is critical to manage impermanent losses for long-term success in DeFi. While IL has been able to exist in most AMM designs, there are various methods to limit or protect against it.

Selecting the Right Pool

- Stable coin pairs: You can provide liquidity to Stable coins like USDC/USDT or DAI/USDT. Because Stable coins are pegged within a very small amount of value, and therefore experience nearly no Price difference between each other, there is little to no impermanent loss; in addition, the fees you may earn from this liquidity tend to have smaller variance and be more consistent than what you may earn in more volatile assets.

- Low volatility pairs: You can also choose to provide liquidity to closely correlated tokens and assets with historically low levels of Volatility. For example, providing liquidity in wETH / stETH Pools will allow you to provide liquidity to two assets that have a high expectation of tracking each other’s prices.

- Single-sided liquidity with IL protection: Some newer projects have created protocols to try to provide LPs with single sided liquidity and/or to protect against IL. Most of these models are incredibly complex, involve different mechanisms of insurance or floor pricing, or ways of dynamically rebalancing LP positions, so you should do your own homework to ensure you understand exactly how the underlying mechanics work and what costs may be incurred when using them.

Hedging with Derivatives

Sophisticated LPs can also utilize derivatives in order to hedge against the price risk of assets they are providing liquidity against and mitigate the impact of IL.

- Shorting One Asset: If you are providing LP to the ETH / USDT pool and were to open a short position against your long position in an ETH derivatives market, should the price of ETH fall, the profit that you would receive from your short position could offset any losses you may incur on your liquidity position due to IL.

- Options: If you purchase a put option on the more highly volatile asset of the pair, should the asset decline significantly in price, your put option will gain value and offset any IL that may be realized through your LP. In developing this strategy, it is very important to manage strike prices and expiry dates carefully.

Tools for Active Management & Monitoring

- Calculators for Impremanent Loss: If LPs use an impermanent loss calculator at regular intervals, they will know how exposed they are with the potential for loss.

- Monitor Divergence in Price: LPs are encouraged to watch the market closely for divergence of the price of their pool's assets. There are monitors that provide real-time data and subsequently alert LPs after large differences have occurred in the price ratio of the two assets in a pool, which helps them greatly.

- Concentrated Liquidity Rebalance: Actively rebalance the ranges in which you provide or receive liquidity for protocols such as Uniswap V3 is a key part of managing your impermanent loss. By actively rebalancing and reactivating your ability to earn fees, LPs will be able to eliminate some future impermanent loss by bringing the prices back within the range of where they are providing or receiving liquidity.

Arbitrage Scanner - A Tool for DeFi LPs to Obtain Useful Market Information

To provide liquidity successfully, LPs must always have access to current market information. The ArbitrageScanner is primarily a tool LPs can utilize to find opportunities to make arbitrage; however, it also provides valuable insight to LPs regarding impermanent loss when providing liquidity. Specifically, LPs can utilize the ArbitrageScanner to help LPs identify the price differences between CEXs and DEXs and how LPs can utilize this information to arbitrage between the two. By utilizing that information, LPs are able to make adjustments to their concentrated liquidity pools based on the price discrepancies identified by the ArbitrageScanner—for example, if the price of ETH/USDT at a larger than 0.5% difference exists across CEXs and DEXs, LPs can use the ArbitrageScanner to evaluate timely adjustments on the range of concentrated liquidity they provide in that liquidity pool, or the timing of when to enter or exit that liquidity pool based on current market conditions.

Conclusion

Impermanent loss is an unavoidable part of providing liquidity to the DeFi marketplace for LPs. LPs need to understand the mechanics of IL and how to calculate and implement strategies for mitigating IL to achieve sustainable profitability. Success in liquidity positions is a function of the relationship between fees earned by the LP and the IL the LP incurs. LPs with access to tools that provide real-time information about the market can make better-informed decisions.

- The difference in value between holding an asset in an AMM versus holding an asset alone is the IL.

- The term "impermanent" means that the IL can be reversed if the prices of the assets return to their original ratios.

- Trading fees may offset IL, but if the price of the asset is highly volatile, the LP will be unprofitable.

- Using concentrated liquidity can create greater potential returns or increase an LP's exposure to IL, which requires an active management strategy.

- LPs can mitigate IL through stablecoin pools, low-volatility pools, and derivative strategies.

If you want to use this information to be informed and make data-driven decisions about your LP strategy, be sure to look into the features available on ArbitrageScanner.

Frequently Asked Questions

What is impermanent loss in layman's terms?

Impermanent loss occurs when an LP provides liquidity to a DEX (decentralized exchange) and the price of the assets in the LP's DEX pool has changed since the time of the LP's deposit into the pool. The LP would have a higher dollar value for the combination of the deposited assets in their wallet than they would have if they were to redeem from the DEX. Impermanent Loss, or the term, refers to the fact that you could eventually realize your "loss" by taking your liquidity out of the market before the asset price returns to its original price ratio.

How to Calculate Impermanent Loss

You will need to calculate the difference between the amount of value you had in assets outside of the pool versus after price changed and they were put back into the pool. For pools that are equal (50/50) it is difficult to find an equation to calculate an exact amount of what a price change (P) will be, but the equation can be approximated to be 2 * sqrt(P) / (1+P) - 1, if you were to double the price of 1 of the 2 assets (P=2) your impermanent loss will be approximately equal to 5.7%. You can find a less complicated way to do this by inputting information into online calculators that calculate what is the impermanent loss.

Will liquidity providers who experience impermanent loss lose out on earning a profit?

Not all the time, as long as you earned more in fees from the trading activity than you "theoretically" lost to the value of your assets. Many liquidity providers who are successfully providing value accept a certain level of impermanent loss if the fees they earn are enough to keep them in profit when added to these "theoretical" losses. It is important for liquidity providers to find the right balance between the two types of losses.

How does concentrated liquidity increase the impermanent loss?

With concentrated liquidity, LPs will provide liquidity to a pre-set range of prices as we see in Uniswap V3. This type of concentrated liquidity helps liquidity providers be more efficient with the amount of capital they have to use and in addition to being more efficient at utilizing their capital; they will also earn a higher amount of trading fees while price remains within their set price range. Since LPs using concentrated liquidity will have their liquidity assets locked in at the end of the range until prices return back to the range, concentrating liquidity may increase their impermanent loss when the prices fall outside the price range set at the time of providing liquidity.

What are some of the best ways to control the risk of impermanent loss?

Liquidity providers cannot prevent experiencing impermanent loss altogether due to the way AMM pools are built, however, there are different things liquidity providers could do to help mitigate their impermanent loss such as:

- Choose stablecoin pairs that have the lowest price deviation.

- Use pairs that experience low volatility and have a high correlation, for example a pair that consists of stETH/ETH.

- Adjust the ranges of your concentrated liquidity to actively manage the impermanent loss you experience.

- Use shorting options to hedge on perpetual futures exchanges to create a hedge against the asset that has the potential of experiencing substantial impermanent loss.

- Constantly monitor the price movement in the marketplace as well as make sure to use tools such as ArbitrageScanner to get a better understanding when to enter or take your liquidity out of a pool.

Want to learn more about crypto arbitrage?

Get a subscription and access the best tool on the market for arbitrage on Spot, Futures, CEX, and DEX exchanges.

You might be interested

Crypto Trading Bots Comparison: 20-Day Profit Challenge

SMT Divergence

DeFi Portfolio Trackers