Crypto Funding Rate Arbitrage: Complete Strategy Guide 2026

with ArbitrageScanner!

Funding Rate Arbitrage can be defined as an investment strategy that does not require you to have an opinion about the future price of the cryptocurrency you want to arbitrage. Funding rate arbitrage uses the periodic liquidity payments made by perpetual futures exchanges to ensure that the pricing of their futures contracts are in line with the underlying spot market for similar financial assets. For example, during an upward trend in the cryptocurrency market with a high number of leveraged long positions, payments from longs to shorts can be as high as 0.05% to 0.1% for each 8-hour period. This creates an opportunity to profit from Funding Rate Arbitrage.

To execute a crypto funding rate arbitrage trade you will need to open two offsetting positions simultaneously, on two different exchanges, maintain your margin and manage your risk while understanding how the strategy can either break even or fail. Every investment strategy has one or more risk/failure modes; however, this strategy has more possible risk/failure modes than 90% of all other strategies currently in use.

This guide will provide you with a detailed analysis of the mechanics of the crypto funding rate arbitrage strategy as of 2026. The following information will be presented: A description of how the funding rate works, the math behind the funding mechanism, an example of what will happen if you have $10,000 and you use two of the largest cryptocurrency exchanges (including estimated net expected returns from the strategy), and a thorough description of the risk/failure modes of this strategy.

What Is the Crypto Funding Rate Arbitrage Strategy?

Perpetual futures contracts do not have an expiration period like a quarterly future; therefore, they need a process that continually keeps the futures contract pricing connected to the price of the underlying asset. The price of the underlying asset throughout the year will typically be considered by the traders making price predictions. The funding rates help to accomplish this.

Every 8 hours on most major exchanges the two parties will pay each other based on the performance of their contract. When the price of the contract is above the spot market price of the underlying asset (such as when retail investors are coming in to trade long under price predictions made by previous traders), the party holding a long position (buyer) will pay the party holding a short position (seller). The funding rate enters negative territory when the markets become bearish and short selling dominates, resulting in shorts having to pay longs.

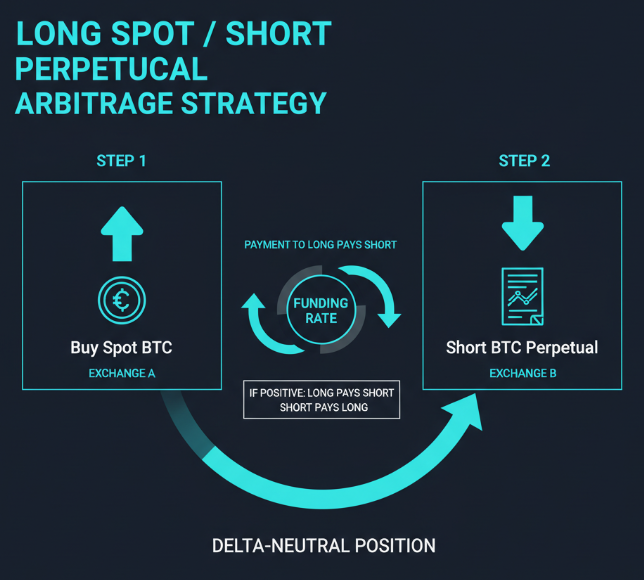

Funding rate arbitrage leverages this phenomenon by taking a delta-neutral position: you buy the asset on the spot and simultaneously sell (short) the equivalent notional amount of the asset on a perpetual futures exchange. By taking both sides of the transaction, you effectively cancel out your price risk. For example, if BTC goes up 10% in value, you would have made approximately $1,000 on your spot position while having lost approximately $1,000 on your short perpetual position, resulting in an effective net price risk exposure of almost zero. The only remaining item of value is the periodic funding payment that you receive as the short party on the perpetual.

This strategy has many names, including basis trading, carry trading, and cash-and-carry, but the underlying mechanics are the same. The primary bet is that the funding rate remains positive long enough for it to drive more value than your aggregate trading cost.

What It Is And How It Works: Mechanical And Mathematical

Summary: Long Spot / Short Perpetual

To execute this strategy, you must take two parties to the transaction at the same time with their respective notional amounts of value equal to each other:

- Spot Long Position: Buy the asset on a spot exchange — you will own it directly, not just your equity.

- Short Perpetual Position: Sell the equivalent value of the asset short on a perpetual futures exchange.

For example, if you wanted to trade BTC at $60,000 and are allocating $10,000 total for the transaction, you would execute approximately the following with your allocated funds:

- Buy approximately 0.0833 BTC using $5,000 on a spot exchange and then simultaneously short (using the remaining $5,000 at 2x margin) $10,000 of notional value of BTC/USDT on a perpetual futures exchange.

This will effectively offset each of your positions to net out the cumulative impact from each position moving independently of each other. When you realize a 5% rise in Bitcoin, you will earn approximately $250 in your spot position while losing about $250 in your short perpetual position. Thus, the positive and negative movement from price will yield a net profit and loss of close to zero. The rate that you will collect from the rest is called funding.

How Funding Rates are Calculated and Paid

It's an easy calculation:

Funding Payment = Notional of Position X Funding Rate

For example, if the BTC/USDT perpetual funding rate on Bybit (a trading exchange) at the time of writing is 0.01% (which has generally been the average during moderate bullish trends), and you have a notional short position of $10,000, the calculation would be:

$10,000 X 0.01% = $1.00 for every 8-hour interval (there are three 8-hour intervals in a single trading day).

If you have a notional position of $10,000, you will collect $3.00/day or $21.00/week or approximately $90/month, all of which excludes trading commission costs. Variables affect resets to the funding rate at the end of each 8-hour interval such as changing sentiment in the market, therefore, this is only an example of how you might receive dollars via this strategy.

During periods of strong bullish trends (as evidenced by the trend in late 2021 or January 2024), the BTC/ETH perpetual funding rate on most major exchanges often exceeded 0.05% to 0.1% per 8-hour interval. If funding were at a rate of 0.1% on a $10,000 notional position, you would earn at least $10/8-hour interval or $30/day, and if you annualized that amount, it would exceed 100% — however, these high funding rates are likely to decrease rapidly as arbitrage capital floods into long positions.

Capital Required for Strategy and Cost Structure

Minimum Capital for This Strategy

Ideally, you should not utilize less than $2,000 to $3,000 to implement this strategy. Low dollar-sized accounts typically have a disproportionately high amount of dollars paid in trading commissions because the cost to enter and exit one round-trip transaction (i.e., buy then sell spot plus open then close perpetual) will cost you approximately $15-$30 for a $5,000 notional account if you trade at actual (i.e., not synthetic) market rates. Therefore, if you have a funding rate of 0.01%, and you pay approximately $20 in trading commissions to open and close a round-trip transaction at an actual price, then it would take you approximately 15-30 positive 8-hour funding intervals to recover your costs if you held your position five or more days (or approximately seven or more intervals). The perpetual leg of a short requires a margin account. If you short $10,000 notional at 2x leverage on futures (i.e., you have $5,000 in collateral) and have a potential loss until the opposite spot hedge is in effect, you also need margin to cover your potential loss during the gap (which are liquidated).

Capital Requirements

You will typically see a return with the funding rate exceeding transaction costs for capital between $10,000-$25,000 required for this strategy. Assuming:

- 0.01% funding rate can be expected to return $1-$2.50 profit above transaction costs per time period

- Less than 20% of the expected monthly funding income will be comprised of entry/exit fees

- You will not have excess cash in the margin account to cover your potential margin until ownership of the hedge arrangement is established

Transactions above $50,000 are no longer a material percentage of returns, and the primary factors become persistence in funding rates and management of liquidation. For capital allocation, approximately 50/50 between the spot exchange and futures margin, minimum of 20-30% on the futures margin.

Example: $10,000 on Binance and Bybit - Step-by-Step

Assumptions: $10,000 in USDT, BTC Price $65,000 and BTC/USDT perpetual funding rate at Bybit is 0.02% each 8 hour period (bull market) for long hold 7 days

1. Identify Opportunity: Find BTC/USDT at Bybit funding rate for last 48 hours, 0.015 - 0.025 % each period. The funding rate has followed a steady trend, indicating an opportunity to enter a trade.

2. Transfer Funds to Binance: Transfer $5,000 in USDT to buy 0.07692 BTC at $65,000. Taker fee of 0.1%, $5.00 for transaction costs. Stage 3 - Open a Perpetual Short Position with Bybit Transfer $5,000 of USDT into your Bybit account to use as margin. Now open a short BTC/USDT perpetual with a total value of $10,000 using 2:1 leverage at Bybit. The total taker fee is 0.055% ($10,000) = $5.50.

Total Entry Fees would be $10.50.

Stage 4 - Receive Funding Throughout the 7-Day Funding Period Use an average performance rate of 0.018% for the total number of days in the funding period (21 intervals) to collect:

$10,000 x 0.018 x 21 = $37.80 in Funding.

Stage 5 - Close Position at Flat BTC ($65,000) Spot: Sell 0.06943 BTC at $65,000, deducting $5.00 fee, receive $4,995 net proceeds. Perpetual: Closing short position at $65,000 results in $0 price (Profit & Loss) - Fee = $5.50, giving $0 Net proceeds.

Total Exit Fees would be $10.50.

Net result would be $37.80 Funding - $10.50 Entry Fee - $10.50 Exit Fee = $16.80 profit on the $10,000 (0.17% Weekly), which is about 8.8% Annualized and slightly below average stable moderate rate environments.

Next, I will provide an alternative scenario where BTC increases in price by 5% ($68,250).

Stage 6 - Same Scenario but BTC Price Increased by 5% to $68,250 Spot: Sell 0.06943 BTC at $68,250 = $5,250 - $5.25 fee = $5,244.75 Net +$244.75 gain. Perpetual: Closing the short position at $68,250 (from $65,000) results in a total loss on the position (Total P&L on Perpetual) - (Total Fees) = $10,000 * 5% ($500 Loss) - $5.50 (Fees) = -$505.50 Net.

Basis Risk Lost: +$244.75 - $505.50 = - $260.75 Basis Risk Loss, due to asymmetrical short leverage and total fees exceeding spot gains.

Funding: $37.80, but total funding - $222.95 gives a loss.

Classic example of the basis risk in which a delta neutral structure can mitigate price risk but does not eliminate it. Further, if the market moves volatility beyond 2 to 3% in between the two buy/sell orders, it is more likely than not that total funding income earned during the funding period will be entirely overwhelmed. Mitigation: Maintain position duration based on your position margin buffer and track the perpetual mark price in relation to your liquidation threshold on a daily basis.

Profit Projections

- 0.005% to 0.02% stable funding rates in a stable market gives you a 8% to 18% annualized return on capital deployed once fees are paid.

- Under bullish conditions, the funding rate could increase to 0.05% to 0.1%, giving you a 55% to 110% annualized return just from funding during the same time period.

- These types of funding conditions typically last less than 1-4 weeks before arbitrage traders bring rates back to affordable levels.

Example of a $10,000 position over a 30-day period:

| Market Condition | Avg Funding Rate/Interval | Gross Funding | Net Funding After Fees | Estimated Annual Yield |

|---|---|---|---|---|

| Low/Stable | 0.005% | $45 | $15 | 1.8% |

| Normal/Mildly Bullish | 0.015% | $135 | $105 | 12.8% |

| Elevated/Strongly Bullish | 0.05% | $450 | $420 | 50.6% |

Note: These are only estimates and are contingent upon wave one realizations. Your true yield will depend upon the fee tier you paid, volatility of the funding period, and the timing of your entries/exits.

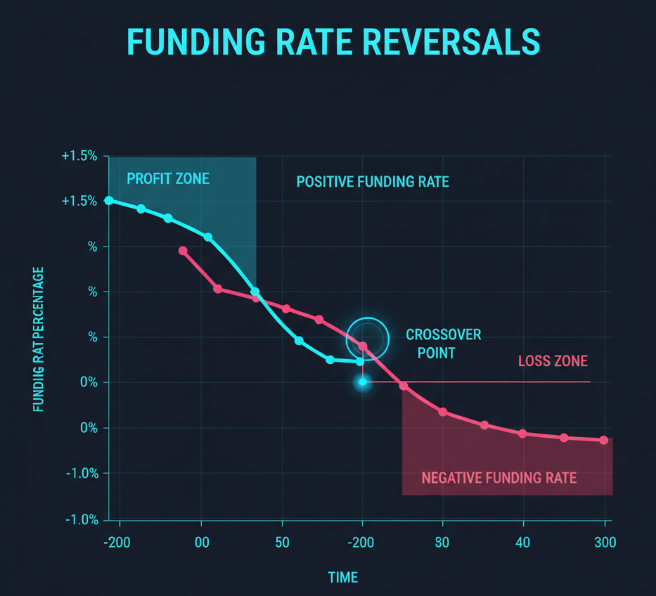

Failure Mode - Funding Rate Reversals

Funding rates show us the current sentiment in the market; they can change wildly within hours of a large sell-off or forced liquidation cascade. When funding rates are negative, your short perpetual position pays the long-term participants – thus, your source of income becomes an expense. You can opt to close the position (pay exit fees), reverse it to take advantage of negative funding rates, or hold onto it until the funding rate turns back positive, with the hope of making enough gains during that period to offset your expense.

Liquidation Risk

Delta-neutral does not mean liquidation-proof. Each short perpetual has a liquidation price. If the price of bitcoin (BTC) goes up sharply (spikes), your futures position may get liquidated before you can transfer/execute an equal amount of spot bitcoin collateral against it to cover your future perpetual trade loss/cost (i.e., to replace what was used from your account as collateral). Maintain a minimum margin of 25%–30% of the value of the futures position as excess margin (above the margin requirement) at all times; this is not negotiable.

Exchange-Specific Risks

- Withdrawal delays or freezes: Moving funds from one exchange to another can take anywhere from 30 minutes – several hours, depending on the exchanges involved. Therefore, a rate opportunity could disappear in transit.

- API failures: The automated position-monitoring systems fail silently when the exchange's API is either throttled or taken offline due to peak market volatility, i.e., during the exact moment they are most needed.

- Fee Schedule Changes: A 0.02% increase in the taker fee for executing a trade significantly changes the breakeven levels on any given trade for accounts with a total value under $25,000.

Slippage and Fees

At the larger notional amounts ($50,000+), placing a market order on either the spot market or perpetual market causes the market price to move away from your expected price. For instance, if one were to buy $50,000 worth of BTC in limited volume (thin market condition), they might incur 0.05% to 0.1% in slippage. This means that you would remove (correct) your position of a commission (commission equals 0 fundings) out long before any fundings that will be accumulated for your position. Placing limit orders can reduce/limit the amount of slippage incurred; however, it introduces timing risk to fill (i.e., if the market moves and the orders aren’t executed before the price moves).

Basis Risk (Improper Hedging)

As demonstrated in the example above, a 5% price movement of BTC renders a $244 profit (spot gain) versus a $505 loss (perpetual loss). If this were considered normal, then a gap of this size is uncommon. During Flash Crashes or Short Squeezes, there can often be as much as a 1-3% basis differential between the perpetual mark price and the spot price i.e. Basis Risk. With such extreme basis differentials, traders would need weeks of positive funding (basis) to recover their drawdowns, depending upon the magnitude of price and time differential.

Black Swan Events

Exchange Insolvency, Stablecoin De-Pegging or Regulatory Freezes have all interfered with the implementation of this strategy by traders using a singular exchange. Diversifying capital across 2-3 exchanges will help to reduce (not eliminate) tail risk.

Top Exchanges to Execute Funding Rate Arbitrage

Exchanges providing the largest liquidity for this strategy include Binance, Bybit, OKX and Bitget for major pairs (BTC, ETH, SOL). For broader altcoin funding opportunities, KuCoin, MEXC, Gate, and BingX provide access to these coins and a larger number of tokens. If you are looking for on-chain alternatives without KYC, Hyperliquid and Drift offer decentralized perpetuals, assuming different liquidity profiles and also requiring smart contract exposure. Key Criteria for Selecting Arbitrage Trades:

- Timing of payments: The quicker the payments (e.g., every 1 hour or every 4 hours), the faster you can compound your gains and the sooner you will be able to exit when the rates turn (increase or decrease).

- Fees: Understanding how much you pay in maker fees is especially important when your account has a notional value greater than $25K, because the difference between maker fees and taker fees will greatly impact your ultimate net return.

- Reliability of withdrawals: If you plan on making a large withdrawal, first, perform a couple of small test transfers to confirm how quickly and reliably the exchange will process your money.

- Documentation of APIs: Having up-to-date, comprehensive, and easy-to-understand documentation about the API will help you monitor your holdings programmatically.

Due to the great depth of liquidity and highly competitive fee tiers, combining the spot leg on Binance and the perpetual leg on Bybit or OKX is a very common practice.

For example, if the Bybit BTC/USDT funding rate is 0.04% and the Binance funding rate is 0.01%, the scanner will immediately show that you have an opportunity to profit on an arbitrage trade because of the discrepancy in the rates between the two exchanges. In addition to the current funding rates, the scanner also displays the trend of the past few periods so that traders can determine whether the most recent spike in funding will still be present when they execute trades on the exchange.

Conclusion

Arbitrage trading in the funding rates generates real returns, but they require active management, diligent tracking of the associated risks, and appropriate documentation for the trades. Here are five steps for approaching your funding arbitrage trades successfully:

- Start with $2,000 — $5,000. It is advisable to have an amount that allows you to understand how margin fees and funding work together, before scaling to a more meaningful or substantial amount.

- Use a funding rate scanner to identify assets where the funding rate has been positive for 48 hours and higher. Do not chase one-off spikes for a single interval.

- Maintain 25% to 30% excess margin on your short perpetual position at all times. Thin margins are the most common cause of liquidation for a soundly constructed strategy.

- Set a minimum funding rate (in your mind) when deciding to stay in the trade. Once the funding rate drops below 0.005% per interval, the position is most likely no longer efficient in covering your fees, and you should close the position before it becomes negative.

- Split your capital into at least two currency pairs on different exchanges. Concentration of capital on a single exchange significantly increases exposure to platform risk. There have been many occasions where traders have been prevented from withdrawing from one of their trades due to a withdrawal freeze.

Frequently Asked Questions

Is Funding Rate Arbitrage Risk-Free?

No, while the delta-neutral structure of funding rate arbitrage has low directional price risk, liquidation risk, sudden reversals in funding rates, basis divergence, and exchange-specific failures create actual loss scenarios. Traders who treat this type of trading as risk-free will often learn their lesson on the first significant market move.

How Often Are Funding Rates Paid?

Most exchanges, such as Binance, Bybit, and OKX, pay funding every 8 hours (three times a day). Some exchanges, such as Bitget and BingX, pay funding more frequently (every 4 hours or 1 hour). Receiving funding at more frequent intervals increases the speed of returns compounding and how quickly one is at risk of a funding rate flip.

What Is the Minimum Amount Needed in Capital to Do Funding Rate Arbitrage?

In practical terms, an amount of capital between $2,000 and $3,000 would allow most of your funding to be retained after fees. With less than $1,000, the cost of an entry and exit round trip can exceed a week’s worth of normal rate income; therefore, one will be mathematically worse off than if these trades had not been executed at all.

Can You Lose Money When Doing Funding Rate Arbitrage?

Yes. The most common loss scenario is a continued reversal of the funding rate. You enter the trade when it was positive, it suddenly becomes negative, and you pay out more than you receive before closing. This is the most common way to lose money. Additionally, severe price spikes can get your short leg liquidated, which would effectively result in losing your entire future margin on that leg of the trade.

How Do I Identify the Best Funding Rate Trading Opportunities?

When looking for funding rate trading opportunities, you should look at the rates of multiple exchanges simultaneously (Binance, Bybit, OKX are much different) for the same asset. Additionally, you should only look at assets that have been positive for either 24 or 48 hours, rather than chasing a single timeframe spike. If you use a funding rate aggregator, you can quickly find the divergences between previous days across different exchanges, which can save you from manually checking each exchange daily.

Want to learn more about crypto arbitrage?

Get a subscription and access the best tool on the market for arbitrage on Spot, Futures, CEX, and DEX exchanges.

You might be interested

Crypto Trading Bots for Arbitrage: Complete Guide 2026

Binance for Arbitrage: Complete Guide 2026

Binance-Bybit BTC Arbitrage: Spread Patterns, Fees and Execution Guide 2026