Reading Whale Wallets Before a Token Unlock: An On-Chain Pre-Unlock Checklist

with ArbitrageScanner!

Token unlocks create supply overhangs that are predictable, but the question really is whether the unlock recipients are going to sell. There is a way to determine that through on-chain analysis prior to it happening, as you simply watch the wallets of those who receive unlocked tokens and look for transfers to their exchange deposit addresses. You can also look to see if a cliff unlock versus linear vesting affected the tokens received by each recipient, as well as checking to see if funding from a perpetual market has occurred prior to the cliff unlock date.

One week to observe the impacts of token unlocks is the week of June 15 - June 21, 2026, as there are four unlocks with very different characteristics occurring in that time frame close together. SEI, ARB, SPK and KAITO are releasing unlocked tokens at different quantities and prices to the tune of 55.56M ($2.86M or 0.93% of total supply) for SEI on June 15, 92.65M ($7.76M or 1.68% of total supply) for ARB on June 16, a headline event of 900M ($17.83M or 27.08% of total supply) for SPK on June 17 and a smaller amount of 17.6M ($7.4M or 4.49% of total supply) for KAITO on June 20.

While these numbers appear to tell you some of the potential for each of these unlocks with respect to dollars, they do not necessarily correlate with how disruptive the release of these tokens will be to the total float for each token. In fact, SPK's unlock is in total dollar value smaller than that of ARB's unlock despite having a much larger percentage of the float lost to the SPK unlock resulting in less impact than ARB's unlock, hence; experienced traders stopped reading unlock news years ago and only look at the wallets of the recipients instead. The understanding behind the events surrounding token unlocks is a move of permissions for certain wallets to sell, therefore, whether or not the tokens of the recipients will be sold in the market will be determined by the behavior of the holders of these wallets. On-chain data will give you the earliest behavioral evidence of these possible sell events prior to the cliff event.

This article provides information about how to read unlock recipient wallets prior to the cliff event, determine whether or not a cliff unlock was one-time in nature or if the tokens received will have been released over time due to linear vesting as well as providing readers with the early on-chain signals that typically occur before someone sells their tokens once they get their unlocked tokens. A reusable pre-unlock checklist and a brief summary of how funding and open interest confirm or deny the signals being given off by wallets are provided toward the end of this article.

Why Unlocks Matter (and Why Most People Get Them Wrong)

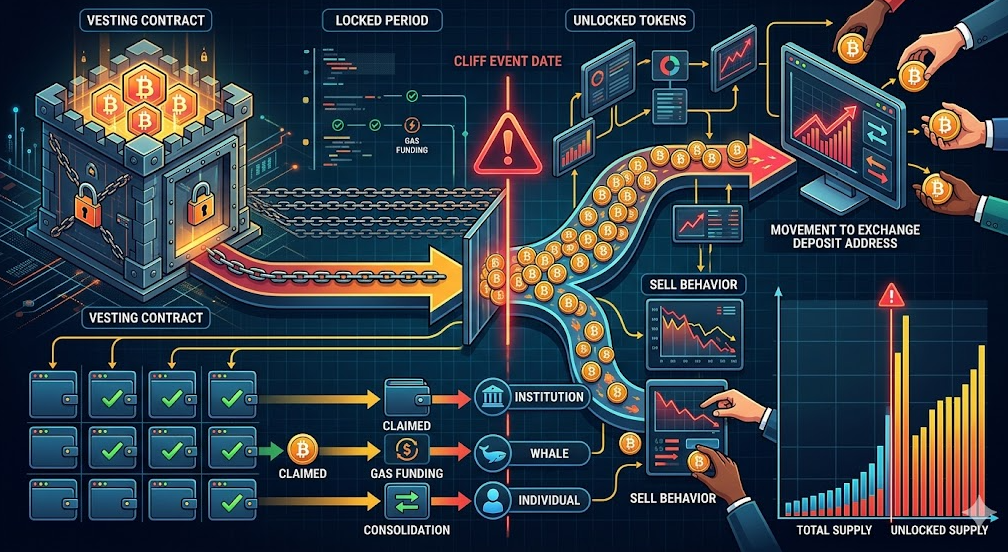

When a project goes live, only some proportion of total supply generally gets circulated while the remaining amount is locked based on a vesting schedule. The lock will expire at a time called an unlock, which can be the date that the lock completely expires or the entire amount becomes available.

If you're a simple-minded model designer, you would probably expect that when new supplies are made available and subsequently become available when new sellers also become available, prices will go down, and you could be missing a lot of real information if you try to make decisions strictly due to what has been or is about to happen. For example, while there is generally some sort of price decline happening at least partially days out from the date of the unlock due to traders front-running the point of an anticipated drop; many events will not occur until the actual unlock has occurred and the token holder does not sell until they know they can sell at a price that allows them to make an attractive profit from their token position. However, this event would still occur regardless of whether a majority or insignificant portion of the tokens being unlocked are actually sold when they are accessible for someone to take ownership of.

In this area, the major insight being provided is that even though the oversupply exists in large numbers, there is no definitive way to know or quantify how many tokens are actually going to be liquidated once the token/s are unlocked. The greatest variables for evaluating whether the market participants will make any significant sales after the unlock events occur include a) who the token holders are and b) what they will do with the tokens immediately after they become available.

In this week specifically, using SPK to evaluate the tokens being released will have a major impact on the market due to the token holder making almost 27% of the total supply available all at once. Adding a supply of this size to the marketplace all at once will create a much larger total supply of tokens that need to be liquidated than what would typically occur across a daily basis through the previous daily volume. ARB and KAITO are both events that are moderate in terms of their magnitude (as compared to other types of events). This means that they can consist of anywhere from less than 0.1% to more than 8%, but the chance of receiving 100% may be more impacted by how a person will behave than by how large the total amount distributed is. In addition, SEI is at 0.93%, so its distribution will consist of very small amounts and will normally contain sufficient noise.

The Difference Between a Cliff and Linear Unlocks

When watching any given wallet, the very first piece of information you need to see is the shape of the unlock you are looking at.

A cliff unlock allows you to receive an entire allocation of tokens in one transaction at a defined point in time. Imagine a flat line that shoots up vertically at the end of the line; it represents one point in time when a recipient has an ability to receive an allocation of tokens. Because cliffs concentrate so much risk at a single point in time, they have the most amount of focus; therefore, recipients who have a plan to sell a cliff allocation usually prepare themselves for this before they can dump their entire allocation into one transaction (which would cause the price of tokens to be very low), because they will want to start dumping their tokens prior to when they actually receive their tokens.

When a recipient receives tokens from a linear vesting schedule, they will continuously be able to receive tokens either in very small amounts (i.e., seconds, blocks, or days) over a defined period of time. The "unlock" event that is posted on the calendar is usually used as a way to account for the cumulative amount of tokens delivered between a defined start and end date; it is not generally used to count how many tokens have transferred from a recipient's wallet. Linear vesting schedules allow for a recipient to sell their entire allocation of tokens through a gradual process instead of a shock to the marketplace.

The operational benefit of these two types of unlocks is:

- For a cliff, the greatest on-chain monitoring window will be from 24-72 hours before the established unlock date; it is during this time that pre-positioning will appear on-chain.

- For a linear vesting schedule, there will generally not be a significant pre-event signal; however, you would monitor the cumulative net token flow from the wallets of the recipients to exchanges over a similar timeframe.

Many large vesting plans include both a cliff for one group and a linear vesting schedule for one or more groups. The first step for each ticker in this week's tickers is to know, by allocation (teams, investors, treasury, ecosystem), whether the June release is going to be a cliff, a linear tranche, or both. Mis-labeling a linear drip as a cliff has become a common tactic among traders to generate fear in the market when the chart has yet to confirm it.

What to Watch for On-Chain Before the Cliff

After figuring out the shape, you should monitor the wallets; here are the most important signals to watch for in order of importance:

1) Transfers to Exchange Deposit Addresses

This gives the strongest signal ahead of selling; since centralized exchanges use individual deposit addresses for each user and when tokens are transferred from a known unlock recipient wallet to a wallet that has historically forwarded to an exchange hot wallet, the intent to sell (or at least have the option to sell) originates before the cliff even fully clears. A cluster of recipient wallets replenishing their deposit addresses for the exchanges within 48 hours of an unlock is also the clearest indication that they were pre-positioning prior to unlocking.

2) Movement From Original Vesting/Distribution Contract

Most of these projects unlock tokens through vesting or claim contracts; therefore when recipients pull out their tokens from the contract as soon as they can, this shows who is paying attention. A wallet that claims and sits is logically very different from the one that claims and routes directly to the exchange.

3) Buying and Selling Patterns for Owners

Sellers planning for an enormous exit typically combine any distributed assets into one entity prior to executing a sale transaction or else divide an extensive token allotment up into many wallets to conceal asset movement and transfer assets to exchanges in separate transactions. In either case, it is worth highlighting that timing of actions to the actual unlock is a key factor.

4) Funding New Wallets to Pay for Gas

If a previously dormant recipient wallet all of a sudden receives a small amount of the default currency used on the chain (e.g., ETH, SEI, etc.) just prior to an unlock, the wallet is most likely being prepared for use. No one puts funds into a gas tank for a car that is going to be unused.

5) Counterparty Reputation

Outflows are not synonymous with sell transactions. Tokens sent to a known over-the-counter (OTC) trading dealer, a market-maker wallet, or an internal treasury address are substantially different than tokens deposited into a retail exchange account. Properly identifying the counterparty position allows for classifying transactions into either an authentic signal or a false one and is the least manual task, which is where classification tools relating to wallets are beneficial.

Summary of Weekly Unlocks

| Token | Date (Year 2026) | Amount (tokens) | Approx. Value of Tokens | % of Total Supply |

|---|---|---|---|---|

| SEI | June 15 | ~55.56M | ~$2.86M | ~0.93% |

| ARB | June 16 | ~92.65M | ~$7.76M | ~1.68% |

| SPK | June 17 | ~900M | ~$17.83M | ~27.08% (largest effect on the total supply during the week) |

| KAITO | June 20 | ~17.6M | ~$7.40M | ~4.49% |

Concentrate more on the right column and less on the dollar value column. SPK is structurally the primary differentiating feature because it has an approximate total of ~27% of all circulating supply changing hands. Should recipient addresses show prevalidation by occupying positions, the supply shock from SEI should not be considered until there is direct evidence from the on-chain activity.

The Pre-Unlocking Wallet Observation Checklist

Have this checklist completed approximately 72 hours prior to any unlock of interest. The purpose is to provide shape-recognition data.

- Verification of Unlock Schedule Shape – What is the shape of the schedule per allocation (cliff, linear, hybrid)? Verify the exact date/time and size of this tranche, not the total size of the allocation.

- Mapping of Recipient Wallets – Determine the vesting contract and the wallets that belong to the team, investors, treasury and ecosystem, and tag each group as per the cohort that they represent.

- Setting a 72 Hour Pre-Cliff Watch Period – If the unlock is a cliff, then this is likely the period of time that you will want to watch for the potential unlocking of these wallets. For a linear unlock, you will want to broaden this out to a multi-day accumulated net flow look-back period.

- Flagging of Exchange Deposit Flows – Any flow from any recipient to a centralized exchange deposit address will be considered your highest urgency flow.

- Monitoring of Gas Top-Ups & Consolidation – Dormant wallets beginning to show activity are likely to be doing something soon.

- Identifying of Counterparties – Separation of any flow heading to a centralized exchange with any flow to over-the-counter (OTC) trade or market makers or treasury accounts is a very important step before labeling any flow as “selling.”

- Quantify Realistic Increase in Supply – Compare the estimated amount of supply to the recent daily off-exchange volume. For example, a 27% of supply unlocked from thin volume is a much larger risk than a 27% of supply that is unlocked from deep liquidity.

- Cross-Reference Sentiment with Perpetual Futures (next topic).

- Identify Your Invalidating Condition – Before you wake up on the date of unlock, create an invalidating condition for how you would consider any body of wallet activity would alert you that an utopia does not exist, so you know not to trade your emotional state.

Interplay of On-Chain Data and Funding/Open Interest Data

Wallets provide evidence of supply intentions, while the perpetual futures market provides evidence of speculative activity and sentiment. The combination of these two data sources is much more powerful than either of them on their own.

Some general trends you can use:

- If there is a significant negative funding ratio leading up to the unlock, that indicates that the market is paying to take a short position to them. An unlock dump may be viewed as a consensus trade that has a high likelihood of experiencing a short squeeze if on-chain selling does not happen.

- When there is a significant increase in open interest and negative funding prior to an OI "cliff," it indicates that there are a significant number of aggressively positioned short sellers. If recipient wallets show no flow into an exchange after the cliff, there is a mismatched supply that warrants monitoring because the expected supply may not arrive.

- If, on the other hand, OI and funding remain flat while a significant amount of value is transferred from recipients to exchanges, it indicates complacency in the market and that recipients are quietly preparing to sell. This is the asymmetry that on-chain monitors typically look for.

The goal of this analysis is not to determine the most likely outcome for a given trade, but rather to potentially identify instances where there is divergence between the wallets acting and the sentiment within the derivative markets. These are instances where potential mispricings exist.

Doing This Without Living in a Block Explorer

Doing this type of analysis without using a block explorer to find and map recipients, identify exchange deposit addresses, and monitor dozens of wallets across multiple blockchains in a 72-hour period per coin is an unrealistic expectation (for 1 token, possibly not realistic and for 4 unlocks over four weeks across multiple blockchains, probably not realistic).

This is why ArbitrageScanner's AI Wallet Analysis engine is able to evaluate wallets based on 272 criteria. It analyzes wallets against hundreds of behavioral signals to identify patterns for insiders, whales, and smart money – including the consolidation, exchange deposit routing, and pre-positioning activity described above – which will allow you to identify recipient clusters that are getting ready to sell without having to manually review transaction history. Together with a listing and unlock calendar, now you can easily see both a forward-looking schedule and live wallet activity in one place: you can know when an unlock occurs and also watch to see if the wallets that received the unlock have sold any tokens.

Our Tools

Some of the elements of the ArbitrageScanner ecosystem are related to this process:

- Wallet scoring – Wallets are scored according to 272 criteria, allowing for the identification of insiders, whales, and pre-unlock positioning.

- Listing and unlock calendar – Get a forward-looking schedule of listing and unlock events, allowing you to schedule your watch windows.

- Coverage – We cover more than 80 centralized exchanges, 25 decentralized exchanges, and 40 different blockchain networks, with second-by-second updates across all of them.

The scanner is fully manual, meaning that it creates signals for you but notifies you of your options because it does not have API access to your account.

FAQ

Does token unlocking always lead to a price drop?

No, token unlocking is simply a process whereby a token can be moved but does not require an individual to sell any of that token once the token is unlocked. In many cases, the markets have already priced the unlock well in advance, and therefore recipients of the unlocks may wait weeks before selling. Market price drops resulting from token unlocking will depend on how the recipient behaves and will be tracked through an on-chain analysis.

What is the best on-chain indicator of anticipated sell-off behaviour by recipients of unlocks?

The strongest pre-positioning indicator of potential sell-off behaviour by recipients of an unlock is the number of times the recipients have transferred tokens from their wallet to the exchange deposit address over a 48-72 hour period preceding the unlock time. Clusters of recipients topping off funds to their exchange deposit addresses during this timeframe should be considered the strongest possible pre-positioning indicators of large quantities of tokens being sold immediately after the unlock.

Why is SPK considered to be the most important unlock this week when it is not the largest dollar amount unlock?

SPK's tokens (about 900 million tokens) represent about 27.08% of the circulating supply of tokens for this week - making this the largest percentage impact for this week when compared to ARB (less than 1%) or KAITO (single digit percentages) or SEI.

How does one identify when token unlocking happens due to cliff unlocks or linear vestings?

The vesting schedule for a project will indicate how an allocation is vested, which can help identify if an unlock is taking place due to a cliff or linear vesting. If a cliff is present, a large chunk of tokens will be released on that specific date, whereas a linear vesting event will release (drip) small amounts of tokens continuously. Events from a calendar in a linear vesting schedule are often cumulative increments instead of one single transaction being issued at that time. Many projects utilize a combination of these cliff and linear vesting schedules.

How does perpetual funding affect the viewer when considering an unlocking event?

Funding can give the viewer insight into how the crowd is positioned in terms of their positioning in relation to the funded traders. If there is a strongly negative funding value (meaning that the traders are paying to be short – as an example) and the recipient wallet is not showing any funds going toward an exchange, then the crowd anticipates a sell off, however, if there is no activity on the recipient wallet, then the trader has a strong probability to incur a loss when selling short. One of the best set ups for this is when the wallet behavior is in contrast to the funding value.

Can I observe all of this activity without using a specialized tool?

There is the potential to observe all of this activity for one token; however, with multiple tokens unlocking in one week, it would not be feasible to do so manually. This is where using automated wallet scoring along with an unlocking calendar would be beneficial.

Try ArbitrageScanner free for one day and see how you like it. Get access to the entire toolkit: including AI wallet analysis on 272 different data points and full access to the unlocking calendar, token unlock dates.

Try out the demo of ArbitrageScanner →

This article is for informational and educational purposes only and does not constitute financial or investment, legal or tax advice. Cryptocurrency trading is extremely risky and can expose all your invested capital to a total loss; token unlock schedules, on chain data and the approximate values used here are subject to change, may contain errors, and should always be verified by the original sources prior to acting on them. On chain signals can provide indications of the possible future behavior of a trader but do not guarantee possible future behavior; and past behavior does not guarantee the behavior of future transactions. ArbitrageScanner is fully manual with no API connection and no access to your accounts. Do your own due diligence and consult with a qualified professional before making any financial decisions.

Want to learn more about crypto arbitrage?

Get a subscription and access the best tool on the market for arbitrage on Spot, Futures, CEX, and DEX exchanges.

You might be interested

Triangular Arbitrage Explained: Profiting from Price Gaps Within One Exchange

ENA Catalyst Rally: Reading On-Chain Signals Before the 20% Move

Hyperliquid–CEX Funding Arbitrage on Long-Tail Perps Explained