Token Unlock Arbitrage: Trading HYPE, ZRO & WET Cliff Windows

with ArbitrageScanner!

Token Unlocks (also known as unlock dates) refer to the set date when locked tokens become available for trade. The term "cliff" refers to a single large quantity of unlocked tokens hitting the market that increases the supply significantly. Because unlock dates are publicly available, the market frequently anticipates selling pressure from unlocked tokens in advance of the unlocks; therefore, it creates, on average, pre-price dislocations between spot and futures, as well as pre-funding swings that a delta neutral trader can evaluate or analyze. This article covers: a breakdown of how unlocks operate; what June 2026’s HYPE, ZRO and WET events taught us; and details of how to monitor unconfirmed token unlocks while using a combination of a futures/funding screener and an estimation of wallet holders to see where unlocked tokens actually go.

What Are Token Unlocks And Why Do They Move Price?

When launching a new project, very rarely does a project exchange all of its token supply with the public at once. Most projects utilize a vesting schedule for the distribution of tokens to team members, early investors, foundations and team incentives over a period of time (typically from several months to several years). Until all the tokens become vested, none of the tokens can be traded or sold.

The best and most recognized example of a token cliff occurs at or near the end of the initial lockup period, which can usually last for six to twelve months. After this cliff, the remainder of that token vest will generally "stream" (out of its locked source) at a linear rate day to day. As a result, the initial cliff is where all market participants will focus their attention because the initial unlock is the largest single event that can introduce significant quantities of additional tokens into tradeable circulation all at once.

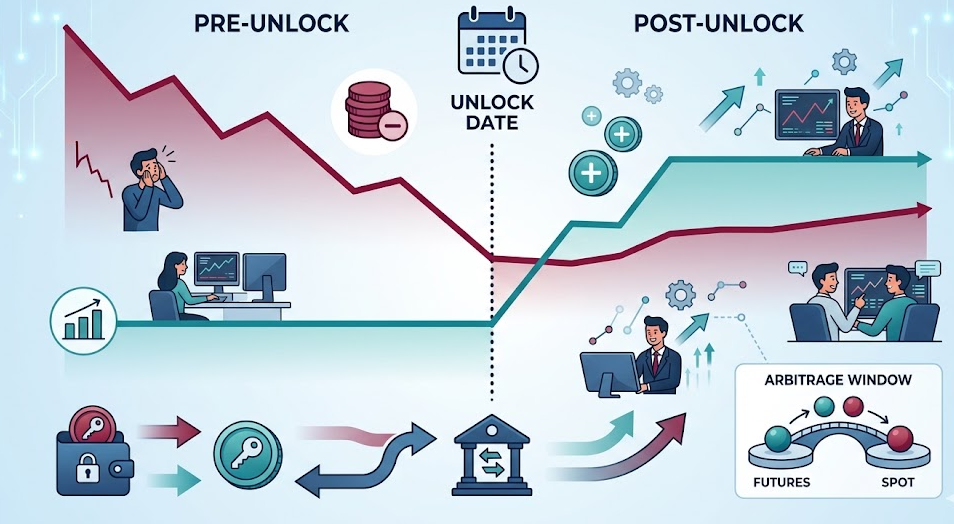

The mechanics of these markets are based on the principles of economics. If you see a large increase in the circulating supply and a flat or relatively stable demand, the last of the new supply will be sold at a lower price than that before the increase. The use of the word will is important because this assumes that market perceptions (forward-looking) will not change during the two periods. Ultimately, the expectation of unlock events has been priced into an asset before the actual date, as they can be publicly tracked on tokenomics trackers.

An unlock is one of the few price catalysts in crypto whose timing is known weeks in advance, which is exactly why the reaction is so often already in the chart by the time the tokens land.

The Three June 2026 Events That Made This Concrete

The mid-June 2026 events all provided opportunities for examining the price action around unlock events, and while many trading opportunities exist around this highly anticipated event, one must understand how they were executed in order to anticipate future opportunities.

Below are three unlock events from mid-June 2026 that illustrate that the expected event price action can significantly vary from the actual price action based solely on the size of the unlock and/or timing with respect to other unlocks (of the same and similar tokens).

| Token | Date | Headline release | The nuance |

|---|---|---|---|

| HYPE | June 6, 2026 | ~$675M cliff (2.54% of supply) | Team committed to claiming only ~$38M |

| ZRO | June 1–7 window | $34.19M unlocked | Mid-sized, steady stream |

| HUMA | June 1–7 window | 26.5% of circulating supply in one shot | Large relative to float |

| WET | June 9, 2026 | 111.59% of circulating float | More than doubled supply in a single event |

HYPE & ZRO

The Unlocked Amount for HYPE and ZRO were similar; however, expectations were significantly different because HYPE’s effective unlocked amount was drastically reduced. The available effective unlocked amount was 1/4 of the effective unlock amount and was primarily a result of a team commitment to claim only ~$38M of the ~$675M cliff amount.

Lessons to be learned:

- Unlock schedule does not dictate unlock sell pressure. A group or individual that indicates they will not sell can convert an alarming headline to a non-event — and possibly a bullish "alignment" signal instead. By year-end, HYPE had already decoupled from BTC and ETH, running significantly higher year-to-date. Consequently, any trader shorter than the headline number that did not first read about the team’s commitment could be fighting both market sentiment and an ineffective thin float to a negative outcome. This is exactly why one does not fight low-float pumps blind.

ZRO and HUMA: what matters is their size relative to their float

ZRO's release of approximately $34.19 million in the same timeframe was mid-sized and digestible as a result. HUMA, on the other hand, released 26.5% of its circulating supply in one single transaction — which was a very large percentage of its float. The dollar value of the release alone is not sufficient to convey the entire message; therefore, a $34 million release occurring on a deep, liquid token signifies nothing, whereas a $34 million release occurring on a thin liquid token signifies an actual supply shock.

WET: this is an exceptional situation where the token supply doubled

WET represents the most highly-extreme situation. The unlock for WET on June 9 was 111.59% of circulating float; therefore, the total number of WET tokens in circulation nearly doubled on that particular date. When the token’s supply doubles, the order book must accommodate a tremendous potential volume of sale activity, and the price discovery process can be highly volatile in both directions. WET, being a low-float token that has just been doubled, represents the typical region of the market where an "obvious" short is commonly squeezed when timely purchasers execute their trades faster than untimely sellers.

The nature of what constitutes an arbitrage window

"Token unlock arbitrage" is a bit of a misnomer; there is no one trade that constitutes arbitrage. Occurrences of dislocations around unlock dates can be categorized as follows:

1. Short selling futures in anticipation of an imminent unlock. Traders take short positions in perpetual futures prior to anticipated unlocks due to negative sentiment towards supply. As a result, perpetual contracts trade at discounted values relative to spot, and the negative interest rate associated with the perpetual contract (the negative funding rate) creates an opportunity for Delta-neutral investors to capture funding by taking opposite positions in spot and perpetual contracts. You can use the spread calculator to size these positions.

2. Mean-reversion of funding rates. Participants often allow emotion and speculation to affect their sentiment before an unlock occurs (e.g., fear of supply). This causes funding rates to fall sharply (often negatively); afterward, when there is no unlock-related news, participants' confidence returns and they revert towards their average level of funding. By tracking extreme funding rates, savvy traders can have insight into the number of participants who are in crowded positions before the reversals of these crowded positions occur.

3. “Sell the rumor; buy the fact” rotation. Since the unlock date is known ahead of time, sentiment often becomes negative well before the date of the unlock, creating an opportunity to get into a long position that experiences the benefit of being able to sell into a local bottom following the unlock (if the unlock is less significant than the market anticipates).

The repeatable edge around unlocks is rarely "price goes down on the date." It is "the perpetual market over-prepares for the date, and that over-preparation shows up in funding and basis."

Framework For Delta Neutral / Short The Cliff

Both an understanding of two types of approaches and not necessarily advice.

Capture via Delta Neutral The Funding

One approach is through “Capture via Delta Neutral The Funding” and represents funding from the current market while not trying to make a prediction on an exact direction for a price movement, since both long & short positions will offset due to their respective price movements, however this type of approach provides only exposure to funding payments (for example: $0.01 funding payment) and then this also allows for anytime a basis between the perpetual and the spot to converge, the basis converged will return a gain since the prior two only provided cost-based returns on funding alone.

There’ll be the potential to create an opportunity to profit when the negative funding rate for shorts increases due to more shorts joining. The risk here is in terms of execution, and you could end up with negative execution imbalance; therefore checking the execution price and size for both legs involved is very important, since you are essentially aligned with the current price movement but also holding your current position with stop losses will determine the success of your position. When monitoring Funding Rates Across Exchanges, when to get in after rates have dislocated as opposed to getting in after rates normalized is a key component to considering benefit during decision making.

Directional Short Cliff

This is more of a risky method whereby traders have positioned themselves a short on certain tokens prior to a token's respective release because they are optimistic that there is more dilution forthcoming than what others have currently perceived and will cause further dilutive effects to the token's price will have a higher probability of success, as shown by how diluted the effective event of June was, by demonstrating their magnitude compared to the float for those tokens (i.e. HUMA-style), or simply demonstrated incorrectly by using HYPE (i.e. HYPE's claim of offsetting the total dollar amount of the effective release) or capital flows moving against them as the perceived float decreases (i.e. WET accident).

The negative annual funding rate associated with holding a short position for an extended period could create risk against your thesis, therefore it is crucial to determine whether or not you will potentially lose as opposed to holding through to see what will occur within the timeframe identified.

Risk management: Don't fight against low floats!

Easy way to think about low floats is: Don't fight against them! When in a low float situation it is necessary to adhere to rules regarding low float situations. Follow these rules for better understanding how to approach low float dynamics going forward. If WET or any token sees its supply double, it could still make strong upward movements if the early conviction holders absorb the liquidity faster than the vested holders can find liquidity by selling.

As with all tokens, size down, set your invalidation level, and do NOT ever assume adding supply = lower price tomorrow. If you want to see how “large” BTC and ETH are, take a look at their completed "unlock" schedules, which were completed a long time ago, creating all-time-high float and little price movement for any single round of vesting (that's why we see unlock-induced dislocations on these thin, recently unlocked tokens).

Watching Where the Unlocked Tokens Actually Go

The most important step is confirming. Although unlocking makes tokens available, it does not mean that the unlock will result in holders of the tokens selling. HYPE is an incredible case study in this gap: $675 million of tokens were unlocked; however, only ~$38 million worth of tokens were actually claimed by an end-user.

Now you may ask yourself, what does on-chain wallet analysis have to do with the above statements? Think about it. With a cliff, you can witness the movement of unlocked tokens from either a vesting wallet to an exchange deposit address (the "holder's intention" to sell) or directly to team and foundation wallets, where the tokens will sit idle. By analyzing wallet transactions with our AI wallet analysis program using 272 different criteria, you will be able to determine if tokens were unlocked but still remain parked, or if they were unlocked and actively transacting to an exchange (the difference between the two examples provided previously is the difference between HYPE and a genuine supply dump).

If you combine the time calendar with trade flow, your guess will become confirmation:

- Examine the token listing calendar and token unlock timetable to see when and how much.

- Examine the funding and basis levels/trends to understand how the perpetual swap market is positioned.

- A Portfolio Analysis can give you an idea of how to analyze the flow of supply in relation to sales.

The three elements of an effective launch of a token, expectations of funding being received from flooding on one side, and the actual flow of tokens on to exchanges create an opportunity for increased certainty regarding the timing of these events between the markets. If one component is not present, the best option to do is to wait for the market to react before proceeding with any transaction.

Frequently Asked Questions

What is a token cliff vest?

A cliff vest is a period of time (currently between 6 to 12 months) that a group of tokens is held without the holders having access to them prior to being distributed in one transaction on some date. Cliff date is the date that all traders are theorizing about because that is the date a large number of tokens will come onto the market at once.

Will the price always decline on the date of unlocking?

Not always; this is due to the fact that the market knows there is an unlock date before it occurs. Therefore, there could be very little or no price decline on the unlock date and/or the price could take off very quickly prior to the unlock date to the extent that the amount of capital expected to be realized upon realization of target sales on HYPE June 6 amounting to $675 million is an example; HYPE's actual offer that day was ~ 38 million; subsequently, no significant downward price movement will occur due to the anticipated sales of tokens expected to be sold on the market (do not have to believe this).

Is short selling against a vendor a reliable method of trading on a cliff?

Shorting is one way to hedge against a cliff-exposed asset; but there may be other methods that are equally or more effective, and there are no guarantees that short selling will work for any or all investors. To assess whether adequate proceeds from a sale will be received due to the unlocking of tokens, it is necessary to consider the number of tokens that will be issued (released) versus the number of tokens that are already in circulation (total market value). To calculate the success of shorting will depend on whether there are also traders who are short; therefore, if there are traders who are short, they will incur the cost of short selling that will be larger than other short sellers, which will result in a greater chance of a lower overall profit. Therefore, low-float tokens are speculative and could cause a substantial loss to any short seller.

What is delta neutral unlocking arbitrage?

Delta neutral unlocking arbitrage consists of selling a cash (spot) price while concurrently facilitating an equivalent long position in a perpetual future (i.e., buy cash, sell open position in perpetual future). This trading strategy will provide opportunity to obtain a profit from receiving funds from funding rates for the spot and perpetual future; additionally, delta-neutral unlocking arbitrage would have the potential to attain profits by taking advantage of a temporary negative ARB from a long and short positions, prior to the unlock.

How do I determine that a token will be sold after it is unloaded?

A great method of accounting for a sale after unloading is to monitor how an established wallet has unloaded tokens from their wallet or account and the amount of tokens that were in the wallets prior to unloading.

For prior to the next batch of tokens scheduled to be released or untradeable, if you are unable to check perpetual basis and funding extremes and on-chain supply, please use Arbitrage Scanner for a free trial period ending with your Telegram account.

Disclaimer: My company only provides information and data regarding trading activities; my company only provides services to those who are at least 18 years of age, have sufficient financial resources to afford the risks associated with using the products of my company, and are qualified investors. This is for informational purposes only and shall not be considered a recommendation or solicitation by my company, its affiliates, or any of its representatives, to use any investment strategy.

Want to learn more about crypto arbitrage?

Get a subscription and access the best tool on the market for arbitrage on Spot, Futures, CEX, and DEX exchanges.

You might be interested

Wallet Intelligence in 2026: Tracking Smart Money With 272 Criteria

Solana MEV in 2026: The Retail Arbitrageur's Survival Guide

Memecoin Listing Arbitrage: The DEX-to-CEX Spread Playbook for June 2026